Am I being charged fees for my plan investments?

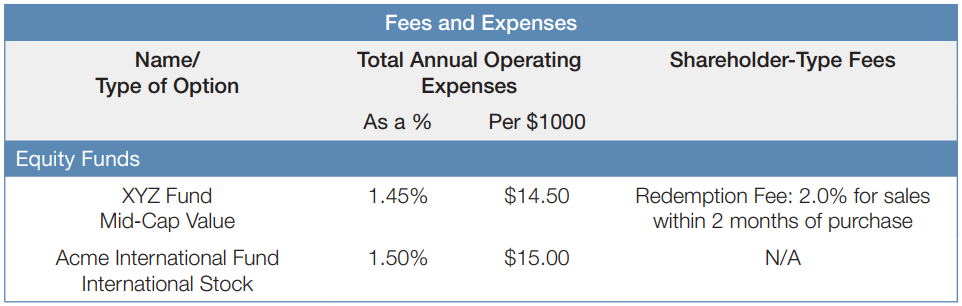

There is a cost associated with operating a mutual fund. This is true whether the investment is purchased through a retirement plan or through another type of investment account. The cost of operating a fund is referred to as the “total annual operating expense” or “expense ratio.” These costs reduce the overall return (the average annual total return) of the fund. Total annual operating expenses will be listed on the comparative chart for each plan investment. It will be presented as both a percentage of assets and as a dollar amount (based on each $1,000 invested). For example, if a fund lists the total annual operating expense as 1.45%, it means that 1.45 percent of the fund’s assets or $14.50 per each $1,000 in a fund will be applied to cover the expenses of operating the fund.

In addition to the costs of operating and distributing a fund, there may also be service charges or fees referred to as “shareholder-type fees” that are assessed when you purchase or sell shares. These fees are typically charged directly to your account and are in addition to the annual operating expenses. For example, a sales charge may be assessed when you initially purchase shares or could be assessed when you sell the shares, referred to as a deferred sales charge. A redemption fee, another type of shareholder fee, is deducted when shares are sold and is paid to the fund to defray the cost of redeeming the shares. For example, a fund that charges a two percent redemption fee for sales within two months of purchase would list that in the shareholder-type fee column of the comparative chart. Some funds also charge other transaction fees to defray cost. In many cases, 401(k) investments will not be subject to shareholder-type fees, and the comparative chart will either be left blank or contain the phrase “not applicable” or “N/A” in the shareholder-type fee column.