Powerful megatrends continue to offer active investors an array of potential long-term opportunities in China

With apologies to Mark Twain, rumors of China’s economic demise have been grossly exaggerated. The mainstream financial media loves a crisis—real or fictitious—and China has been a favorite target. We’ve all seen headlines of a “property bubble” or looming “banking crisis.” But is China’s economy really teetering on the brink of disaster?

Not so fast, argues Mike Reynal, chief investment officer of Sophus Capital. Reynal believes talk of a China meltdown reflects a superficial analysis that misses the point. Rather than focusing on the headlines and GDP numbers, a deeper analysis reveals an economic backdrop with intriguing, long-term opportunities across an array of industries.

Reynal suggests investors take time to ponder the dynamics and longer-term trends before drawing snap conclusions on the Chinese economy.

See the big picture

When China began shifting away from a strict centrally planned economy three-and-a-half decades ago, the massive shift from an agrarian to urban economy was launched. Urbanization, privatization, and the gradual removal of price controls and protectionist policies have fueled lasting job creation. Current GDP growth may be lower than in the recent peak years of 2006/07, but we are only in the middle innings of the megatrend. Today, urbanization continues unabated, and China has publicly stated its goal to help 200 million-plus rural residents transition into new cities over the coming years.

China’s endgame is to transform the economy from a basic, export-driven emerging market to one resembling South Korea—with its impressive services and tech sector—over the next two decades. In order to do so, urbanization needs to rise from an estimated 55% of the total population today to close to 70%. This trend supports a bullish long-term investment thesis.

Think beyond exports

When talking about the Chinese economy, investors tend to focus narrowly on exports and the industrial clusters such as those in Zhejiang and Guangdong Provinces. Yes, exports are important, but they remain a relatively low percentage of China’s growth, estimated at 22% of GDP. This is actually lower than many other emerging export-driven economies, such as Vietnam. Today, the reality is that China is an enormous consumer society with rising discretionary spending and household income. Chinese society does have a very high savings rate, which reflects the lack of liquid investment options and the absence of a social safety net. However, the arrow is pointed upward for Chinese consumer spending. Consumer finance is still in its infancy and the consumer is under-levered. This consumption story remains one of the most powerful investment themes across emerging markets or anywhere.

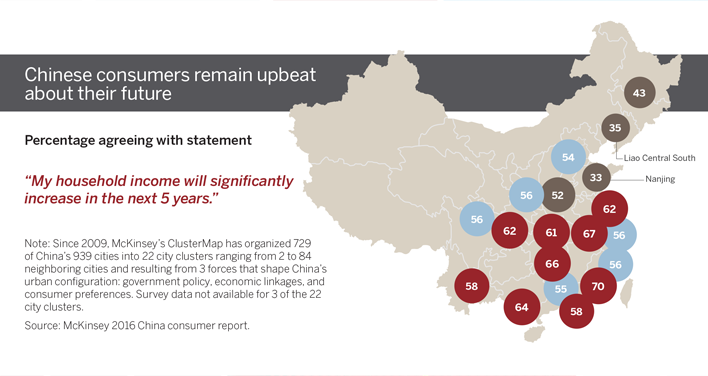

Chinese consumers remain upbeat about their future