The threat to globalization must be acknowledged, but history suggests it won’t be derailed

Chinese President Xi Jinping recently traveled to the World Economic Forum in Davos and championed the benefits of globalization while highlighting the risks of protectionism. Meanwhile, populists in Britain and the U.S.—stalwart nations of global free trade—have been busy talking up the scourge of globalization. It’s an upside-down world only Lewis Carroll would understand.

Indeed, globalization is in the cross-hairs of many politicians these days. Threats of tariffs and protectionism abound, and, if enacted, they could pose a drag on global economic growth. Nobody correctly predicted the political outcomes of the past year, and certainly nobody knows how nationalism will manifest itself in future trade policies. Yet there is a feeling that more sensible minds will prevail and globalization is, ultimately, unyielding. Moreover, any setbacks and subsequent market volatility might provide opportunities for active managers who can capitalize when stock prices disconnect from fundamentals.

History as our guide

Mike Reynal, chief investment officer of Sophus Capital, fully acknowledges that there are very real risks to globalization today. But as an equity manager with a global perspective, he still believes in trade liberalization and its ability to lift both developing and developed countries. He points to statistics from the World Trade Organization that show a longer-term trend of rising international trade following the conclusion of WWII between 1950 up until the Global Financial Crisis. There may be setbacks along the way, and cross-border capital flows may still be below peak levels from a decade ago, but Reynal believes that the slowing pace of trade liberalization and rising protectionism rhetoric is unlikely to completely reverse globalization.

He reminds us that globalization is driven by four key factors: cross-border capital flows, trade, migration, and the free-flow of ideas and communication. Capital flows and trade may have hit a speed bump, but migration and the exchange of ideas and knowledge continue unabated. In fact, the era of digital globalization (the vehicle of increased knowledge-sharing) is still in its infancy, and the Sophus Capital team believes that the amalgamation of cross-border ideas is an unassailable historical force that will continue to propagate globalization in the future.

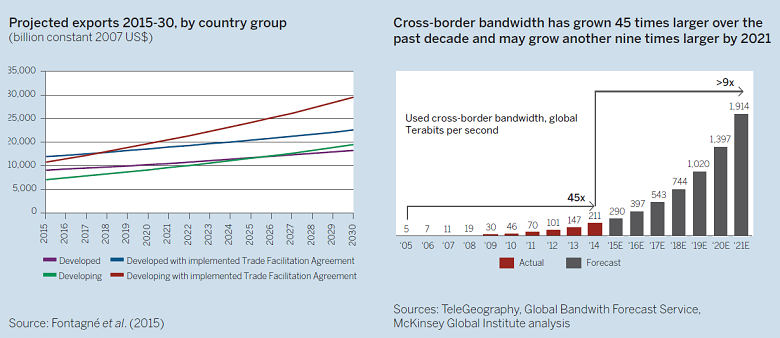

This exchange of knowledge—delivered by rising cross-border data flows—may verify the notion that globalization is indeed inexorable. A 2016 report from McKinsey Global Institute asserts that in contrast to slowing international trade in recent years, digital flows are showing no signs of abating. Cross-border bandwidth “has grown 45 times larger since 2005,” and “is projected to grow by another nine times in the next five years,” according to the report. All of this is boosting participation in the global economy and suggests that globalization is not reversing¹.