The Sophus Capital Emerging Markets Team combines analytical tools and fundamental research to pick equities.

The Sophus Capital Emerging Markets Team combines analytical tools and fundamental research to pick equities.

Much of the developed world is marred by low growth and high debt. That’s not a particularly appealing backdrop for equities, so it should come as no surprise that both institutional and retail investors are keen to explore the far reaches of the globe in order to find that elusive growth.

Much of the developed world is marred by low growth and high debt. That’s not a particularly appealing backdrop for equities, so it should come as no surprise that both institutional and retail investors are keen to explore the far reaches of the globe in order to find that elusive growth.

Although the willingness to broaden one’s investment horizons far beyond the comforts of home is an important first step, dallying in markets with varying degrees of opacity and liquidity is no easy feat. Succeeding in emerging market equities and capturing alpha over multiple economic cycles requires deep experience, uncommon skill, and the right approach.

“Emerging markets are an unbelievably diverse, dynamic, and thriving arena for investors,” explains Mike Reynal, head of the Sophus Capital Emerging Markets Team. “And, in our opinion, picking stocks is the most consistent way to generate excess returns in emerging markets—much more so than country selection, sector rotation, or market timing. Our process combines the powerful aspects of analytical tools with deep fundamental research. We aim to build a portfolio of stocks with superior growth potential at attractive valuations.”

Even for stock pickers who prefer to focus on individual companies, it’s critical to monitor the macroeconomic picture and pay close attention to the various layers of political, sovereign, and currency risk inherent in emerging markets. It can be difficult for investors to access corporate information and government statistics. And although fraud is not exclusive to emerging markets, it is sometimes more difficult to identify than in developed markets.

“We’re undeterred by these challenges because that’s what creates the information gaps and biases that are embedded in emerging markets,” continues Reynal. “For us, that inefficiency spells opportunity, and picking the right stocks from within this dynamic is how we seek to generate alpha versus the benchmark.”

Alpha: a statistical measurement used to quantify the value added or subtracted by a portfolio manager. Specifically, alpha measures the portfolio’s actual return against the portfolio’s expected return given the risk of the portfolio.

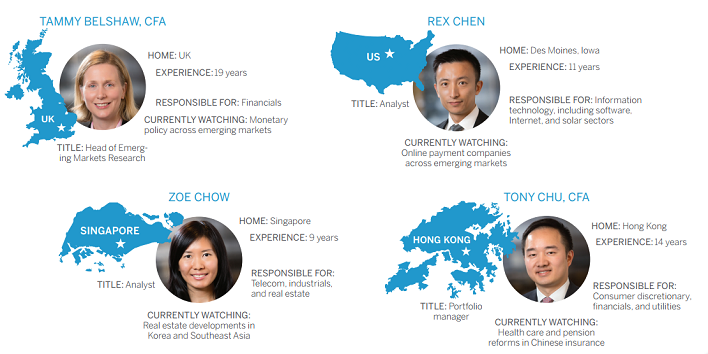

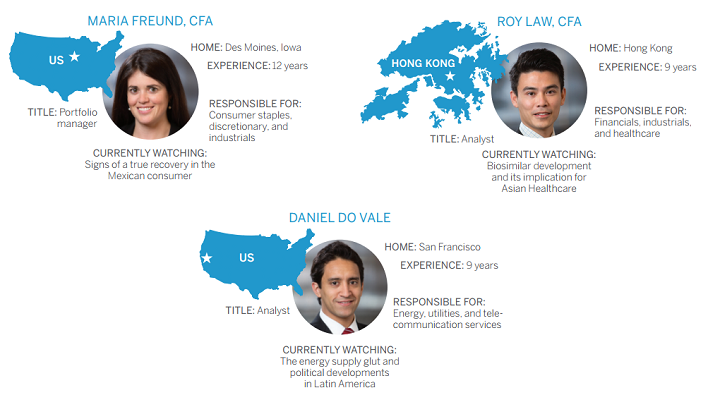

Capitalizing on the potential of emerging market equities takes unique skill. The Sophus Capital Emerging Markets Team is a diverse group of professionals long on experience with a proven process that marries the best of analytical tools with fundamental research. Collectively, the team holds 1,500 company meetings in person per year, not including conference calls. We believe being close to management is critical for understanding both industry trends and individual companies. We think proximity to emerging markets trumps being in a single location. Five of the 10 members are located in Asia, which illustrates the team’s commitment to closely following some of these enormous emerging markets. And when our Asian-based analysts wake up in the morning we want them to read about Sino-Japanese relations first and the U.S. Presidential elections second— not the other way around. Plus, our strict implementation of our investment philosophy encourages us to be in multiple locations and still preserve fluid communication.

The Sophus Capital Emerging Markets Team adheres to a strict investment philosophy focused on building a portfolio of emerging market companies based on four key characteristics: superior earnings growth, attractive relative valuation, improving earnings expectations, and potential for positive earnings surprise. The team believes these are the characteristics of stocks that have the highest likelihood of delivering share price appreciation. And within that universe of stocks, the team is forever committed to paying a reasonable price for above-par growth potential. Discipline and valuation are critical components of their philosophy. “We don’t fit comfortably into a single style box,¹ which is sometimes a challenge for consultants and investors,” admits Portfolio Manager Michael Ade. “We can easily straddle that core-growth space, but the bottom line is that our emerging investment philosophy tilts toward growth even if we monitor valuations very closely.”

The Sophus Capital Emerging Markets Team adheres to a strict investment philosophy focused on building a portfolio of emerging market companies based on four key characteristics: superior earnings growth, attractive relative valuation, improving earnings expectations, and potential for positive earnings surprise. The team believes these are the characteristics of stocks that have the highest likelihood of delivering share price appreciation. And within that universe of stocks, the team is forever committed to paying a reasonable price for above-par growth potential. Discipline and valuation are critical components of their philosophy. “We don’t fit comfortably into a single style box,¹ which is sometimes a challenge for consultants and investors,” admits Portfolio Manager Michael Ade. “We can easily straddle that core-growth space, but the bottom line is that our emerging investment philosophy tilts toward growth even if we monitor valuations very closely.”

The team opts for sustainable growth because that’s what equity markets typically reward. Certainly, value can be a powerful factor and outperform dramatically, as in the post-crisis period in the spring of 2009. But according to the team’s extensive research and back-testing, equity markets usually reward factors such as positive and improving earnings growth.

“Still, we think it’s important to pay attention to valuation and believe that if we buy growth at a discount, we can maximize our potential alpha,” explains Ade. “That’s one of the benefits of our process—the combination of analytical tools with fundamental research can help us buy growth at a discount.”

The Sophus emerging markets philosophy may tilt toward growth, but what really sets the team apart is the systematic way that it goes about identifying companies and building the portfolio. The team uses proprietary, multifactor models to help focus its fundamental research efforts on those companies exhibiting favored characteristics. These screens systematically sift through thousands of stocks every week and indicate where sustainable growth is likely to be available at a discount.

The team ranks the broadest universe of stocks by using these screens that have been developed and back-tested over nearly two decades. These are multifactor models that help identify a number of fundamental and behavior attributes, giving the team a unique ability to cull through reams of data.

This is then complemented by a fundamental, deep-dive research process on individual companies, which leverages the sector and regional expertise of analysts with boots on the ground in that particular geography.

“Every analyst on the team has full visibility of the screens and models,” emphasizes Tammy Belshaw, head of Emerging Markets Research. “This is not a black box and far from a pure quant process. Rather, it’s a fundamental process that leverages very sophisticated and powerful models.”

In investing parlance they carry nondescript names like overconfidence, anchoring, and familiarity. In reality, these are simply behavioral biases that can lead to costly investing mistakes. The Sophus Capital Emerging Markets Team uses its analytical tools to help mitigate the potential fallout from any of the biases that are known to undermine analysts and investors.

By their very nature, models are brutally objective, explains Daniel Do Vale, an analyst on the Sophus Capital Emerging Markets Team. “When a stock falls out of the top quintile, it forces the team to re-evaluate its original investment thesis to determine whether it still deserves a place in the portfolio. The model doesn’t have feelings or an ego. It doesn’t care what price you paid for a stock. It merely highlights a potential concern, thereby forcing a discussion and deeper analysis of the company.”

Conversely, many investors may be predisposed to sell their winners too early. But the team can resist this urge by looking to see how a stock screens even after it has appreciated. If the company is still ranking well, the team will be disinclined to sell. Models are not a panacea, but they can go a long way in helping analysts avoid some of the common psychological investing mistakes inherent in human nature. The models are not a replacement for company research but rather help orchestrate the fundamental process.

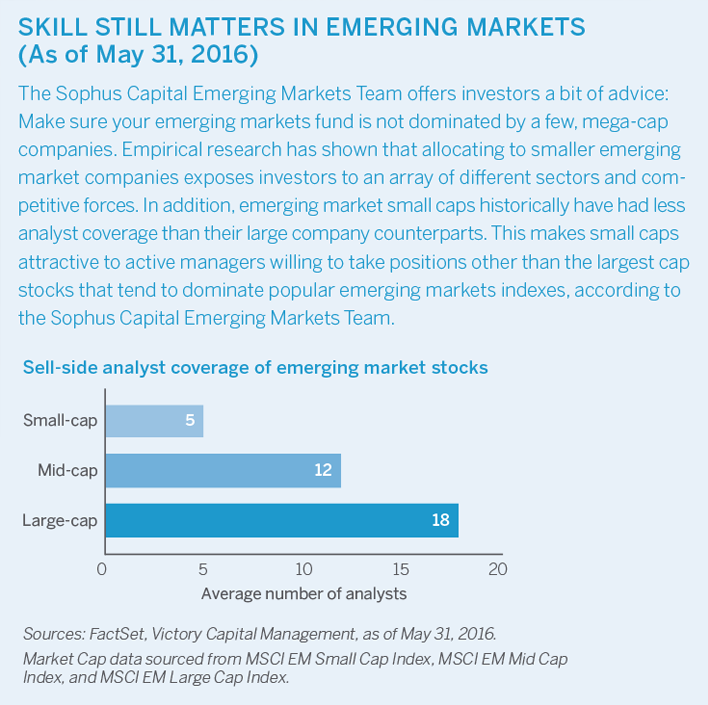

Emerging market managers operate in an expansive universe encompassing 3,300 companies across more than 20 countries. That’s a great deal of ground to cover for any team, no matter how large. Thus, the systematic screening process, coupled with fundamental research, is really about enhancing efficiency and capturing a far wider set of opportunities than would otherwise be humanly possible. “The proprietary models we’ve built simply point us to where inefficiencies live within the markets,” explains Daniel Do Vale, an analyst on the Sophus Capital Emerging Markets Team. “These models rank the most attractive opportunities in a way that an analyst alone cannot.” At the same time, it’s important to underscore the fact that the model does not pick stocks—the analyst does. Any decision on including or jettisoning stocks is based on growth potential and fundamentals. This is why relevant emerging markets investing experience actually matters.

“A screening system alone cannot identify risk on a company level,” Do Vale continues. “What it can do is create a pool of stocks that has more sustainable growth potential. From there, each sector specialist has the opportunity to capture the story and identify the triggers of why we are going to make money from each stock based on both growth potential and valuation analysis.”

Although the Sophus Capital Emerging Markets Team does not invest thematically, a multitude of opportunities are originating from the globalization of trade and growth of a powerful consumer class. There are legions of first-time credit card holders and automobile owners. This is an undisputed megatrend. In addition, outsourcing of manufacturing to the Guangdong Province (and elsewhere) is increasingly being diversified to places like the Philippines, Mexico, and the Czech Republic. With the services sector furthering this outsourcing trend, opportunities are emerging everywhere.

Yet in order to capitalize on these inefficient markets, we believe investors need to be able to overcome their preconceptions and behavioral biases. Again, this is where the models are very powerful because they can highlight areas of the market and individual stocks that most people overlook. And having unique insights is especially important for an emerging markets manager seeking to generate alpha.

Having the tools to capture efficiency and generate investing ideas is essential. But there is no substitute for emerging markets experience. One cannot simply invest based on the output of a model. There’s more skill involved in picking emerging market stocks.

Consider that some Chinese property companies and banks may screen well with their robust growth metrics, but it’s critical to understand that the policy environment trumps all in these sectors. Government-linked decisions and lending mandates can undermine any growth story. Thus, the screening may queue up potential opportunities, but we believe having experience and knowledge of policy, culture, and other local market nuances ultimately dictates success.

Brazilian utilities are another example where government policies could affect minority shareholder interests in the future. A systematic screen may not pick up the fact that the long-term earnings power of an entire sector is being eroded until it’s too late. If you are following a model blindly and don’t follow the political landscape and sector trends, you could find yourself in trouble.

Many emerging market managers prefer to focus exclusively on picking countries, which can be an all-or-nothing proposition. You might be a top performer one year, or you might just as easily find yourself with a bucketful of cheap Egyptian stocks—and getting cheaper. Country picking is a difficult game, so the Sophus Capital Emerging Markets Team prefers researching companies and selecting stocks as a means for generating alpha. Another common mistake made by some emerging market managers is focusing only on the largest and most liquid names. But then again, not many managers use analytical tools in a disciplined way to help them identify hidden, fast-growing companies long before they have a slick investor relations road show. Too narrow a focus is unnecessarily limiting and even risky should sentiment change and investors head for the exits. The Sophus Capital Emerging Markets Team believes it has a better way.

“Early in my career it was drummed into me that you buy emerging markets just because they are cheap,” says Reynal. “But that’s not why I buy them. I buy because I think I can get superior growth potential at an attractive value. And in our current environment, growth is a beautiful thing.”

1. The Morningstar Style Box is a nine-square grid that provides a graphical representation of the “investment style” of stocks and mutual funds. The Style Box defines three size categories (small, mid, or large company stocks) and three style categories (growth, value, and core). Core represents those stocks for which neither value nor growth characteristics dominate.

As with all mutual funds, the value of an investment in the Fund could decline, so you could lose money. International investing involves special risks, which include changes in currency rates, foreign taxation and differences in auditing standards and securities regulations, political uncertainty and greater volatility. These risks are even greater when investing in emerging markets. Small companies may be subject to a number of risks not associated with larger, more established companies, potentially making their stock prices more volatile and increasing risk of loss.

An investor should consider the fund’s investment objectives, risks, charges and expenses carefully before investing or sending money. This and other important information about the investment company can be found in the fund’s prospectus, or, if available, the summary prospectus. To obtain a copy, click here.

The Funds are distributed by Victory Capital Advisers, Inc. (“VCA”), member FINRA and SIPC. Victory Capital Management Inc., an affiliate of VCA, is the investment advisor to the Funds and receives a fee from the Funds for its services.

NOT A DEPOSIT • NOT FDIC OR NCUA INSURED • MAY LOSE VALUE • NO BANK OR CREDIT UNION GUARANTEE

©2016 Victory Capital Management Inc.

R15-1431_ART16Q2_LG

May 1, 2017

February 16, 2017