The Morningstar Category Averages cited below assume reinvestment of dividends.

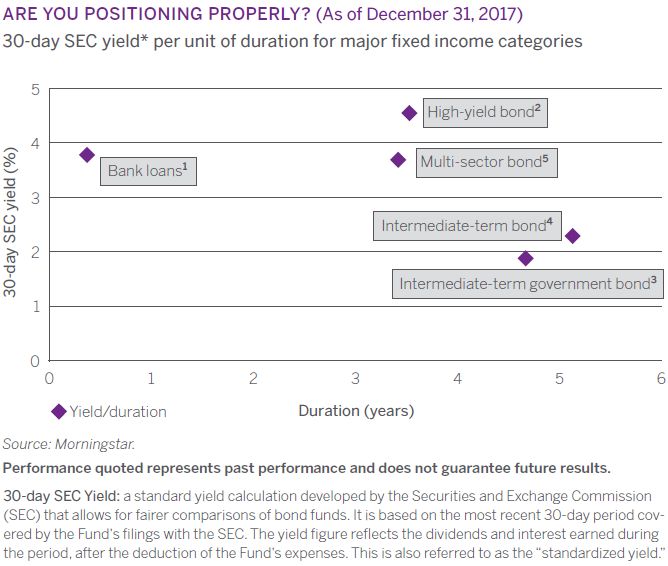

1. Morningstar Bank Loan: Bank loan portfolios primarily invest in floating rate bank loans instead of bonds. These portfolios have credit risk and limited duration risk. The Morningstar Category Average is the average duration and average 30-day SEC yield for the peer group based on the durations and 30-day SEC yields of each individual fund within the group, for the period shown.

2. Morningstar High Yield Bond: High yield bond portfolios concentrate on lowerquality bonds, which are riskier than those of higher quality companies. The Morningstar Category Average is the average duration and average 30-day SEC yield for the peer group based on the durations and 30-day SEC yields of each individual fund within the group, for the period shown.

3. Morningstar Intermediate Government Bond: Intermediate-government portfolios have at least 90% of their bond holdings in bonds backed by the US government or by government-linked agencies. The Morningstar Category Average is the average duration and average 30-day SEC yield for the peer group based on the durations and 30-day SEC yields of each individual fund within the group, for the period shown.

4. Morningstar Intermediate-Term Bond: Intermediate-term bond portfolios invest primarily in corporate and other investment grade US fixed income issues and typically have durations of 3.5 to 6.0 years. The Morningstar Category Average is the average duration and average 30-day SEC yield for the peer group based on the durations and 30-day SEC yields of each individual fund within the group, for the period shown.

5. Morningstar Multisector Bond: Broad bond portfolios that typically invest assets among several fixed-income sectors, including government bonds, corporate bonds, high-yield bonds and foreign bonds. The Morningstar Category Average is the average duration and average 30-day SEC yield for the peer group based on the durations and 30-day SEC yields of each individual fund within the group, for the period shown.

An investor should consider the fund’s investment objectives, risks, charges and expenses carefully before investing or sending money. This and other important information about the fund can be found in the fund’s prospectus, or, if applicable, the summary prospectus. To obtain a copy, visit www.vcm.com. Read the prospectus carefully before investing.

All investing involves risk, including potential loss of principal.

Fixed income funds are subject to interest-rate and credit risk. Typically, when interest rates rise bond values decline. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Securities with floating interest rates are less sensitive to interest rate changes but may decline in value if their interest rates do not rise as much as interest rates in general. Floating rate investments issued in connection with leveraged transactions are subject to greater credit risk than many other investments. Derivative transactions can create leverage and may be highly volatile.

The information and statistical data contained in this material were obtained from third-party sources believed to be reliable; however, Victory Capital does not guarantee the accuracy of the information or data, and the information and data may differ from information provided by Victory Capital. Any opinions, projections or recommendations in this report are subject to change without notice and are not intended as individual investment advice.

The Funds are distributed by Victory Capital Advisers, Inc., member FINRA and SIPC, an affiliate of Victory Capital Management Inc.

NOT A DEPOSIT • NOT FDIC OR NCUA INSURED • MAY LOSE VALUE • NO BANK OR CREDIT UNION GUARANTEE

©2018 Victory Capital Management Inc.

V18.010 // 1Q 2018 VC In Brief: Bracing for higher rates IB