Almost a decade after the financial crisis, the banking sector looks healthy with candidates for growth at reasonable valuations

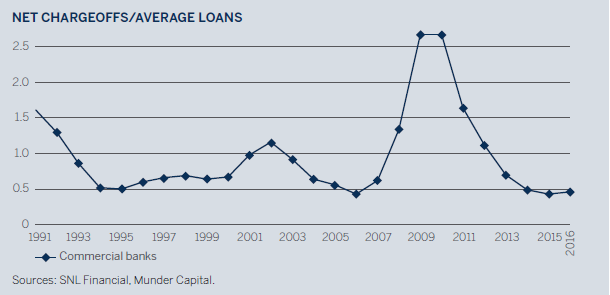

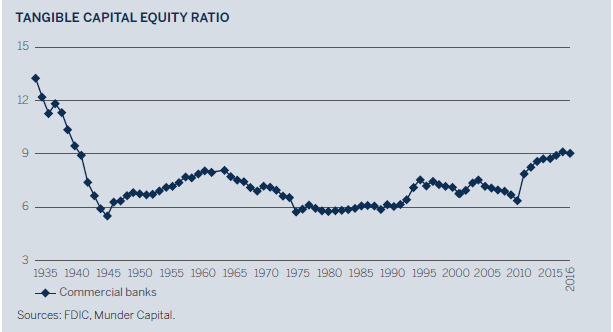

First it was housing. Then, sovereign debt. For a spell, it appeared that banks were simply lurching from crisis to crisis, so is it any surprise that investors have remained skeptical of the sector? But upon closer inspection, much of the turmoil appears to be in the rear view mirror, and the general health of the banking sector has improved materially. At least that’s the opinion of Brian Matuszak, senior portfolio manager with Munder Capital Management, a Victory Capital investment franchise. Closely monitoring the financials sector is among Matuszak’s responsibilities, and from his vantage point he sees several bank candidates poised to deliver steady growth. Among other factors, he cites strong credit quality and bank capital ratios at their highest point since the great depression. This is a great backdrop from which to pick stocks, he says, but as always the balance sheet details matter.

Q: People still remember the last crisis, but you say that the health of banks has changed materially. What do you see?

Q: People still remember the last crisis, but you say that the health of banks has changed materially. What do you see?