Don't be so sensitive

JIM TRACY 10-Oct-2018

Sure, interest rates are low in a historical context, but as of mid-September 10-year Treasuries were once again looking to top (and stay above) 3%. And thanks to the recent robust job numbers, the real questions are not if the Fed will continue tightening, but rather how much further and how fast.

Given that backdrop, investors are right to revisit their fixed income allocations. Will bonds continue to play their traditional role in an overall investment portfolio? And if so, how should investors allocate their fixed income budgets?

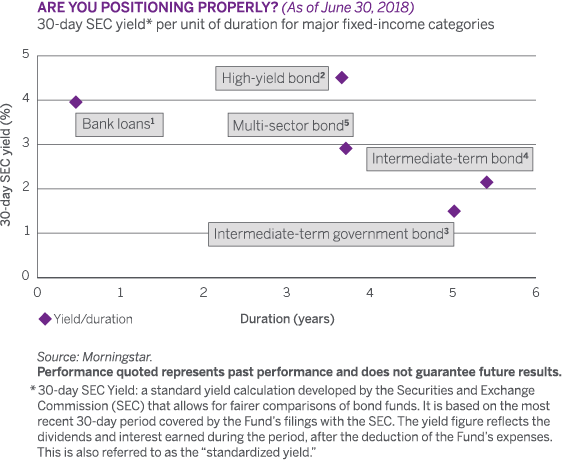

For clues, investors may wish to look at duration. Duration is defined as a measure of interest rate sensitivity—the longer the duration, the more sensitive the investment is to shifts in interest rates and the greater its potential for losses in periods of rising rates. Floating rate bank loans may provide attractive risk-reward tradeoffs as evidenced by duration.

As their name suggests, floating-rate bank loans are variable-rate loans made by financial institutions, generally to non-investment grade companies. Unlike most fixed income instruments, they can help balance an overall portfolio’s exposure to rising interest rates, providing greater price stability when compared with longer-term fixed interest rate bonds. This is due to their variable-rate yields, which adjust periodically, typically every 90 days, to mirror changes in market interest rates.

Moreover, bank loans are often ranked senior in a company’s capital structure, which means that, in the event of a default, bank loans are typically senior to bonds, convertibles, stock and other unsecured claims. In other words, these loans have priority for repayment and access to collateral.

Of course, there is no free lunch, and investors should always be aware of the risks associated with this asset class, including credit and liquidity. In fact, some common push-back comes from investors who wonder whether they are simply replacing duration risk with credit risk. That may be a viable concern given that bank loans are often below investment grade. Yet an active manager with deep credit research capabilities may be able to mitigate that risk by avoiding industries and individual companies with deteriorating balance sheets and higher risks of default. An active manager can also reject investments with inadequate liquidity.

All investments carry risks, but at a time when interest rate risk is increasing, investors should remember that floating-rate bank loans, which can offer attractive yields, are among the few fixed income assets that have the potential to maintain or increase in value in a rising rate environment. From this perspective, bank loans may prove helpful in structuring a fixed income portfolio.