Don't skip lunch: It's time to put risk-weighting on your menu

CAIA & KEVIN BALES, CFA MANNIK DHILLON, CFA 24-Jan-2019

It’s time to put risk-weighting on your menu. After all, diversification is widely considered “the only free lunch in investing.”

Nobel prize-winning economist Harry Markowitz once quipped that diversification is “the only free lunch in investing.” Isn’t it ironic, however, that in challenging periods and at times of market extremes, some investors question the benefits of diversification?

That’s our current environment, and that’s exactly why we continue to advocate for strategies that are disciplined in how they spread risk. This is especially important for any core equity allocation. So to those investors who have been allocating to products that track the cap-weighted S&P 500® Index and have benefitted from the recent tailwind provided by mega-cap stocks—congratulations on your fortuitous timing. Now be wary.

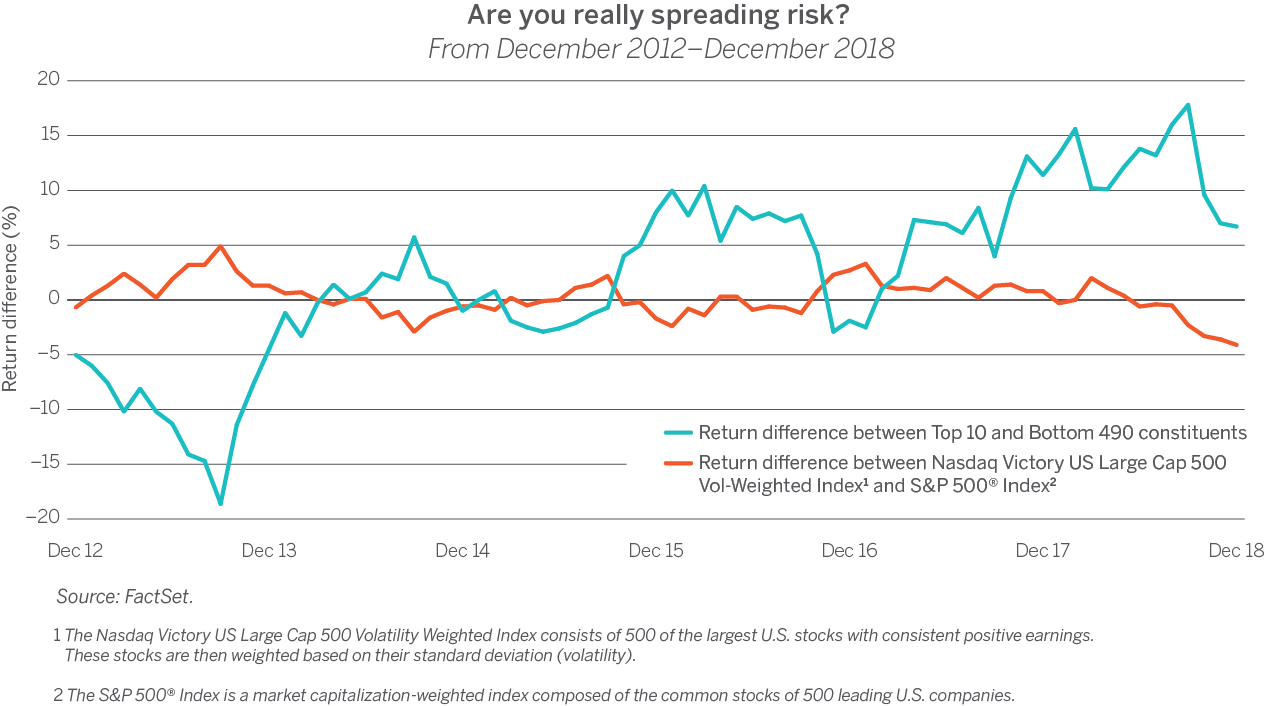

Culminating in 2018, the S&P 500 had become a de facto outsized bet on a handful of mega-cap stocks—specifically technology companies—that dictated the performance of the index. But if history is any guide, investors might want to reconsider such an allocation given current levels of dangerous concentration and what typically transpires after we reach these extremes.

Market-cap weighted indexes are built by weighting individual constituents by size. The larger the constituent becomes, the more it influences overall performance. In 2018, the top stocks of the S&P 500 were dominating the index, and the extreme levels of concentration not seen since the dot-com bubble were elevating its risk profile. In fact, we would argue that the S&P 500 is really just a concentrated bet that is more suited as a tactical play on mega-caps as opposed to a core holding.

Look ahead, not behind

Concentrated pockets of leadership within the stock market are fickle. Remember the“four horsemen in 1999?” The energy sector and financials have also taken their turn with outsized influence in the S&P 500. And most recently the FAANG stocks (plus Microsoft) have enjoyed the limelight. The point is, no one knows exactly when the current leaders revert, but they almost certainly will. It is better to spread risk evenly across all constituents for a core equity allocation as opposed to making a concentrated bet on a few mega caps that fall in and out of favor.

The adjacent graph should be a cause for concern for anyone allocating to the S&P 500. Don’t invest based on what happened last year (or any single year), but rather look ahead and consider how an allocation might perform over the next two to three years, and far beyond.

Looking at the current situation, it appears that a cap-weighted benchmark like the S&P 500 may be vulnerable to a period of underperformance relative to a more diversified approach. Investors in the S&P 500 should be looking forward given the recent levels of performance concentration and wonder if and when we will see a reversion.

Seeking true diversification

For those investors who are considering an equal-weighted index methodology for their large-cap allocation, we would suggest thinking twice. In fact, equal weighting the S&P 500, for example, naively over-allocates to smaller companies within that large-cap universe as a means to generate better returns. But equal weighting is inherently flawed because it extends risk in order to achieve a small performance bump, and there’s no guarantee it will be successful at that.

Rather, we think true diversification is the better approach. This may not be obvious every single year, but it may likely hold true over time. So if you believe you should own less FAANG, less concentration and be more diversified, it might be time to consider pivoting to a risk-weighted approach for your core equities allocation. We believe the VictoryShares solution—one that screens for consistent profitability and spreads risk more evenly across the portfolio—is appropriate for the long haul, not only for large-cap domestic stocks, but also across small caps, emerging markets, and international equities.