Equities: A guiding light

Lance Humphrey, CFA & Michael Mack 15-Aug-2025

Many investors have been unnerved by market volatility during the first half of 2025, thanks largely to all the uncertainty surrounding tariffs, geopolitical turmoil, and other factors. In this challenging environment, we think there is one overarching principle that can help investors manage volatility and identify companies positioned for success. Free cash flow (FCF) can be foundational for building durable stock portfolios, in our opinion.

Simply stated, FCF is the amount of cash a company is generating after paying all expenses incurred to fund operations. We think that companies with excess cash flow tend to be well positioned to grow their businesses or otherwise fund shareholder-friendly activities (such as stock buybacks, dividends, repaying debt etc.).

Why do we like FCF as a barometer? Companies with high free cash flow have more self-funding reliance, which is especially important given the current macro backdrop of higher interest rates and risk-averse lending. Also, companies rolling over expiring loans may find new terms less favorable, which can be troublesome for those that rely too heavily on debt to fund operations and growth. By contrast, companies with ample FCF should have an edge in terms of strategic flexibility.

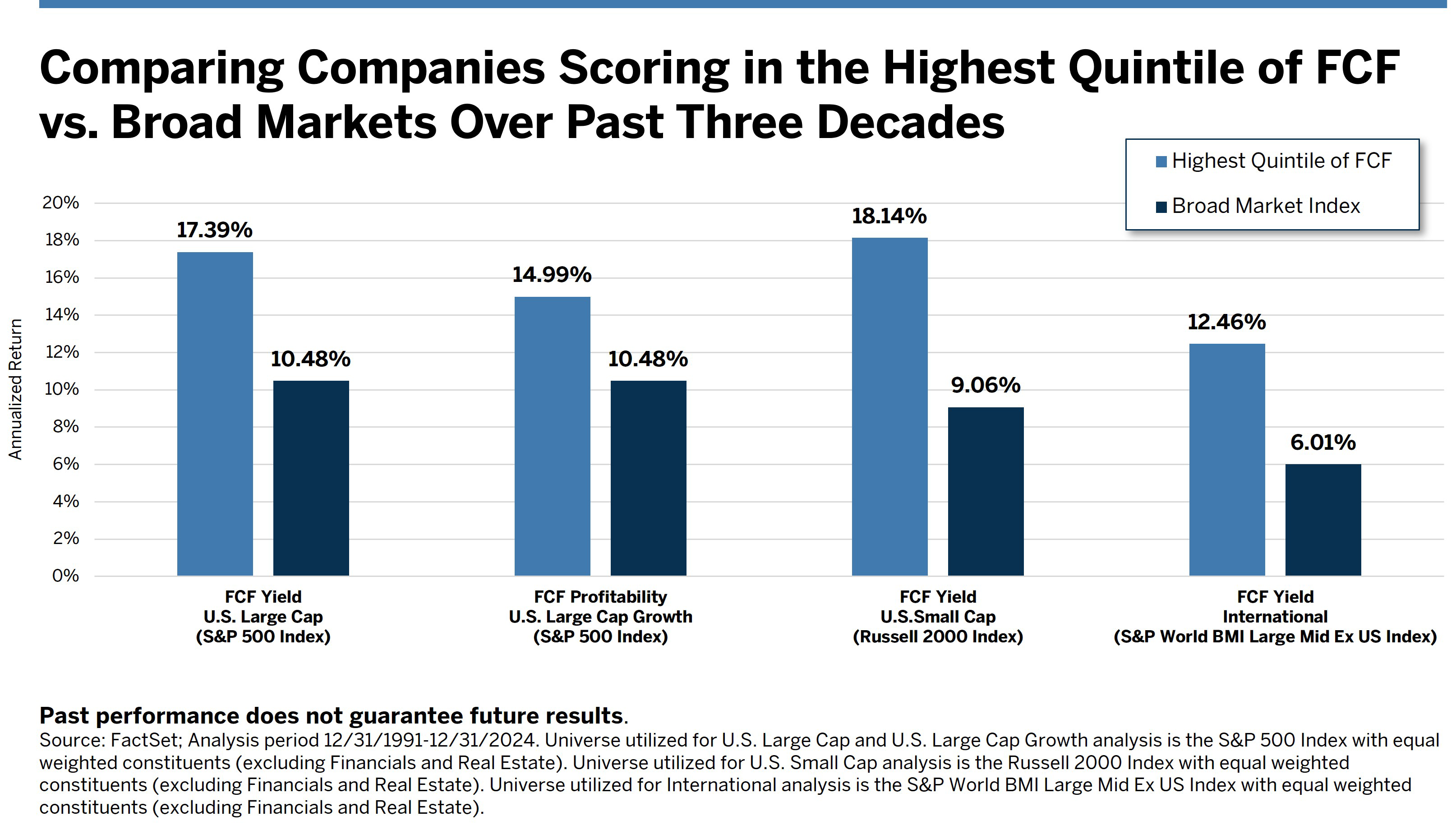

FCF Across Investment Styles

Our research has shown that FCF has efficacy across many investment styles. In fact, one might argue that it can be used to build core equity allocations in both growth and value style boxes; for small- and large-cap equities; and for international equities as well. For evidence, the following graph shows how companies with high FCF yield (value)—which is a ratio that compares a company's free cash flow to its market capitalization—and FCF profitability (growth)—which is a ratio that compares how efficiently a company uses invested capital to generate FCF—have performed versus the broader market.

Importantly, we believe that investors should also consider a forward-looking measure of FCF, as opposed to relying solely on a historical measure of FCF, which has been an industry norm. That’s an important distinction. Looking both forward and backwards when analyzing FCF reveals a more complete picture, in our opinion.

When it comes to using FCF to help build an equities portfolio, we want to reiterate that we believe there’s no need to limit it to large-cap domestic equities. Plus, if market leadership continues to broaden out and move beyond a narrow cohort of mega-cap stocks, we think a diversified FCF approach could be especially effective. Thus, if historic and future FCF is a harbinger of company health and share price performance, why not consider applying it broadly in today’s environment?