Equities: If the bucket begins to leak

Christopher Cuesta, CFA & Manish Maheshwari, CFA 03-May-2024

First it was the “FAANG” stocks. Then the spotlight expanded to include the “Magnificent Seven.” But whatever we choose to call them, there’s no denying that the domestic stock market has been dominated by just a handful of names. Over the past several years, these mega-cap companies have enjoyed remarkable success and share price appreciation, and they have been largely responsible for the impressive gains of the S&P 500®, which is the most common used proxy for U.S. stock market.

Many investors who use ETFs or mutual funds that track the S&P 500 benefited from the index’s rise to all-time highs during the first quarter of 2024. But is there a cautionary tale here as well? What happens if the mega-cap bucket starts leaking? If there’s a reversion to mean valuations between the largest companies in the U.S. and the rest of the market, does that leave some equity investors vulnerable? We think that question is worth asking.

In revisiting portfolio allocations or in conjunction with any rebalancing, investors and their advisors might step back to consider if it’s appropriate to shift some capital a bit further down the cap spectrum. Specifically, we see the mid-cap asset class as offering an attractive risk-reward trade-off, particularly given its legacy of long-term performance.

Not Middling

Why do investors seem to favor large-cap stocks when building core portfolios? Perhaps it’s their familiarity with some of these pillars of the U.S. economy. Perhaps it’s just because the S&P 500 is often cited in the press, and the long-term performance of that index has been “good enough.” Yet many investors might not realize just how top-heavy that index has become. The index may include 500 companies, but it is cap weighted, which means that each index constituent is weighted relative to its total market capitalization, or size. In a cap-weighted index when a few companies are so much larger than the rest, the performance will be driven by this handful of stocks. That’s the case with the S&P 500. As of the end of the first quarter 2024, the 10 largest constituents in the S&P 500 represented a whopping 34% of the index.

This concentration has been a tailwind recently, so investors have been mostly unconcerned. But at some point the stock market rally will shift. This might leave core equity allocations based on the S&P 500 more vulnerable to a steep drawdown (or simply mired to a decade of treading water, as was seen between 2000 and 2010).

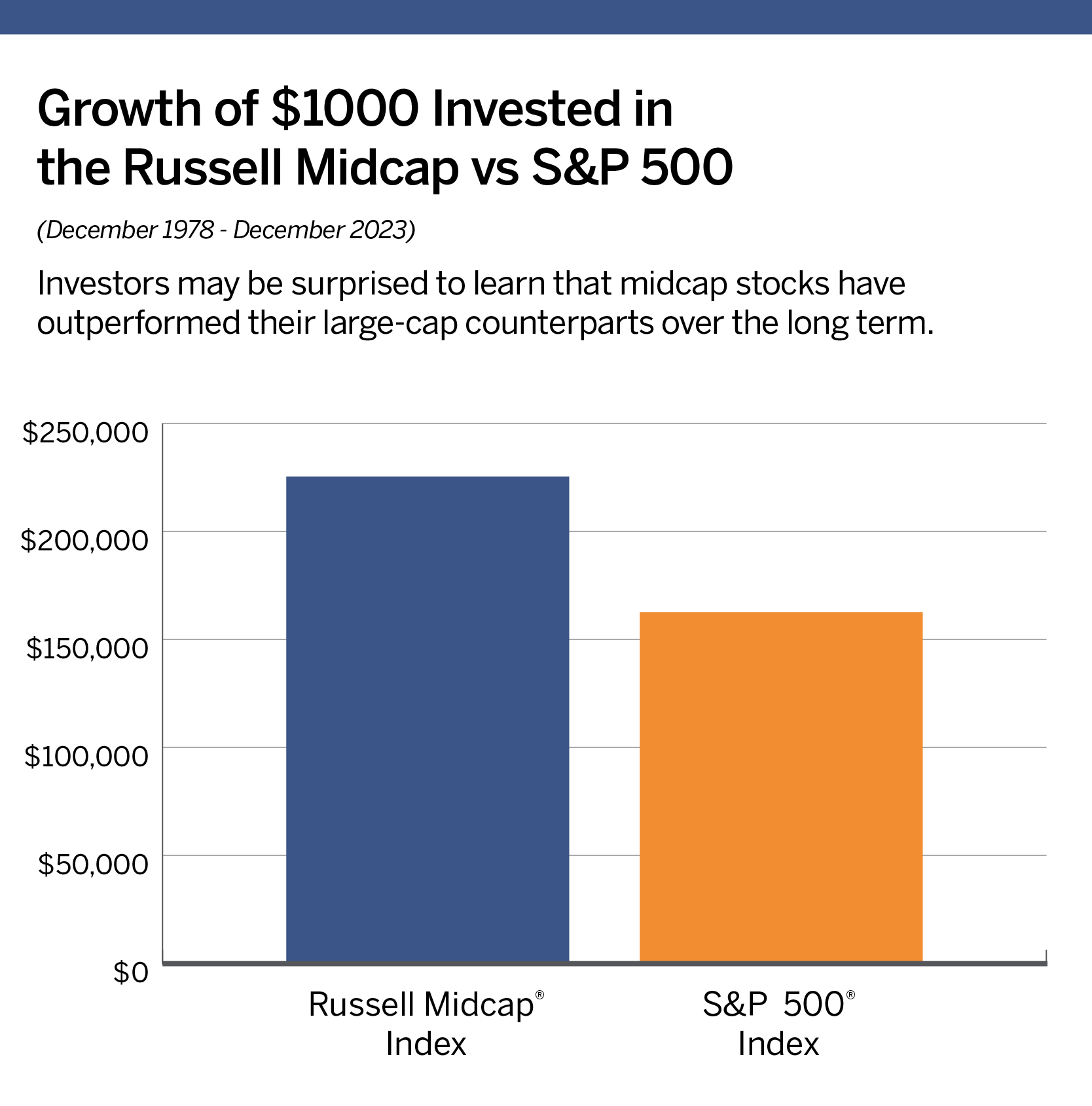

One possible way to address this concentration risk is by broadening out and allocating to equities further down the cap spectrum. Not only will this enhance diversification, but it might also improve the long-term return potential of a portfolio. Many investors will be surprised to learn that mid-cap stocks have outperformed their large-cap counterparts over the longer term. The graph below illustrates this point using two common benchmarks for large and mid-sized stocks.

Source: Russell Investments, S&P Gobal, THB Asset Management

We all know that past performance is no guarantee of future returns. But we have looked back even further to study performance over various market environments and across multiple economic cycles. Looking at the rolling 10-year returns of large-cap stocks versus mid-cap stocks using CRSP* indexes dating back to the inception of their data in 1925, mid-cap stocks have outperformed large caps an impressive 75% of the time.

Acquisitions & Organic Growth

All this begs the question: What exactly has been behind this longer-term performance of mid-cap stocks? We think it’s reflective of a handful of characteristics inherent to the asset class.

For starters, we like to own companies that we think are at the sweet spot of their lifecycles. Startups and other fledgling companies often have funding challenges and execution issues. Slightly more mature companies, like mid caps, are beyond their formative years but still tend to have a long runway of potential growth.

Furthermore, we see the ability to combine acquisitions and organic growth as a powerful recipe that might be partially responsible for their impressive longer-term performance. According to our analysis, the companies within the Russell Midcap® Index have acquired a staggering 18,732 companies, valued roughly $5 trillion, over the past 20 years ended December 2023. Acquisitions are one way that these medium-sized companies can quickly enter new markets, expand their product bases, and, if executed properly, boost revenues and earnings growth.

Finally, our research also shows that mid-caps have outperformed inflation in every decade. This might be especially relevant today given the recent spell of elevated inflation data that may prove to be “stickier” than the Federal Reserve hopes.

Active Management & ETFs

Another key reason for us to like the mid-cap landscape is that it appears to be a less efficient asset class compared to large caps. We believe there is institutional underinvestment in the space, as well as fewer analysts covering a wide swath of stocks. This creates an environment where share prices may not properly represent the true value of company assets. Such a dislocation opens the door for fundamental active managers to find attractive risk-reward trade-offs, in our view.

Importantly, investors now have a growing ability to access actively managed mid-cap equity strategies using ETFs. Marrying the potential of the asset class with the advertised benefits of ETFs, which include tax efficiency, liquidity, and daily share price discovery, may make sense for many investors.

Ultimately, investors may be right to consider whether their core equity allocations are overexposed to just a handful of very large companies that may be richly valued. One possible corrective action could be to shift the focus a bit further down the cap spectrum and consider the role that mid-cap stocks can play over the long term. That might be worth considering, particularly if the mega-cap bucket ever starts leaking.

* The Center for Research in Security Prices (CRSP) provides financial and economic data and indexes to academic, commercial and government institutions.