Equities: Mind the middle

Christopher Cuesta, CFA & Manish Maheshwari, CFA 04-Oct-2023

Large-cap companies—many of them popular household names—have enjoyed a strong run in recent years. These companies garner much attention in the media, so it’s easy to understand why they are top-of-mind for investors. Yet many may be surprised to learn that mid-cap stocks have outperformed their large-cap counterparts over the longer term. And now, given current valuations as well as the inherent characteristics typically associated with mid-cap companies, many investors might ask: Should mid-cap stocks take on a more prominent position in a diversified equities portfolio?

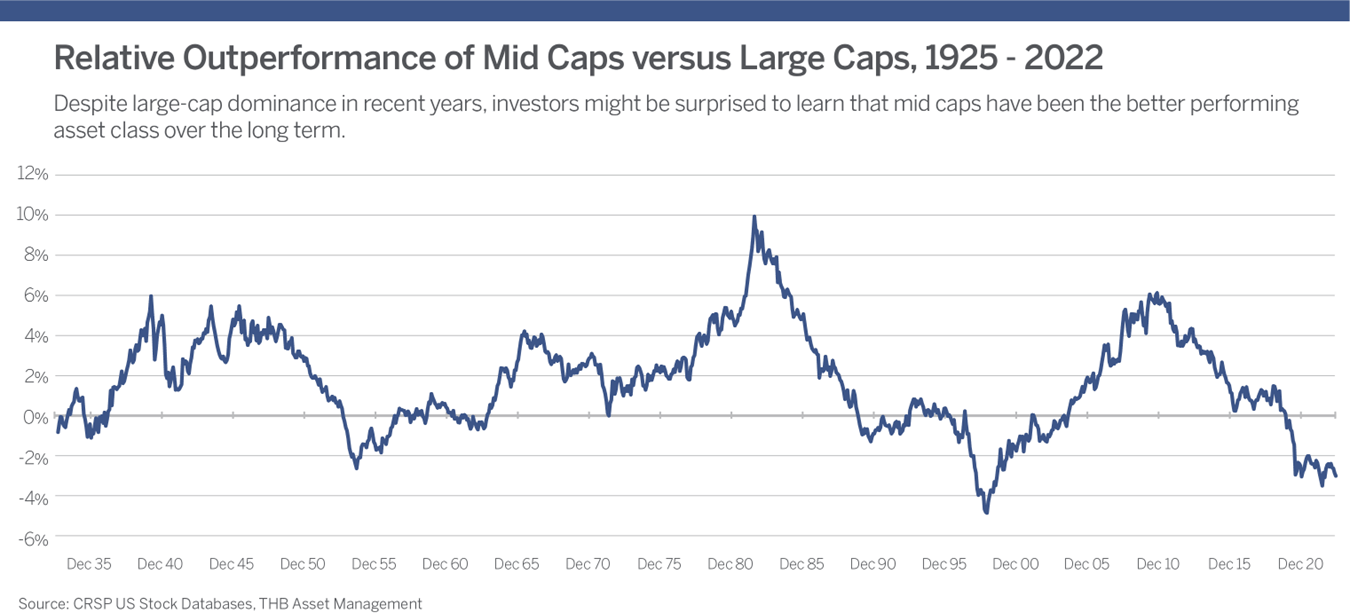

THB Asset Management offers one especially compelling bit of data—the rolling 10-year returns of large-cap stocks versus mid-cap stocks using CRSP index data. The graph below illustrates the relative outperformance of mid caps dating back to the inception of the data in 1925. Over this very long time horizon, mid caps have outperformed large caps an impressive 75% of the time.

Moreover, this leadership position has tended to shift back and forth in extended cycles. Savvy investors might derive that it is opportunistic to allocate to mid caps after a period of underperformance versus their large-cap counterparts, particularly if there is any mean reversion. It’s also worth noting that the current underperformance of mid caps versus large caps has only been worse one time since this data has been published—in the hey-day of the dot-com era in the late 1990s. If the equity markets “normalize” as we expect, it would not be surprising to us to see mid caps begin a period of outperformance.

Of course, we all know that history is no guarantee of future returns. But there are more reasons to like mid-cap stocks beyond past performance and relative valuations. For starters, THB Asset Management likes owning companies that they believe are in the prime of their life cycles. Mid caps, by definition, have passed their formative years and are perceived less risky than small fledgling companies. Younger companies, even with innovative products or disruptive business ideas, face greater risks executing their business plans and continuing their growth trajectories. Many mid-cap companies have overcome these early challenges yet still offer a long runway of growth potential, and they typically have better access to capital markets given their maturity and track records. This point should not be overlooked in late 2023. Today’s tighter monetary conditions and prevailing interest rates that may be higher for longer make access to (cheap) capital a critical factor for growth and success.

Another perceived advantage of mid caps is their ability to grow both organically and by acquisition. These companies can blend characteristics of early-stage growth companies, but with the experience, stability and access to capital that can allow them to opportunistically acquire firms to enter new markets or otherwise take advantage of synergies and economies of scale. For example, a mid-cap company might be able to create value by acquiring a complementary product and leveraging an existing robust distribution channel to capture new revenue streams. This could be a great driver of earnings growth and, ultimately, the company’s share price.

In terms of absolute size, mid cap stocks also might offer an advantage. Consider the denominator effect. Is it easier for a behemoth with a market capitalization approaching $1 trillion to double its revenue, or a smaller company earlier in its lifecycle? This seemingly simple mathematical reality should not be discounted when comparing the opportunity set of mid caps to large caps.

Finally, it’s important to remember that mid caps are a relatively inefficient asset class. There are a greater number of obscure mid-cap companies and fewer analysts covering mid caps than their large-cap counterparts. Moreover, we see broad underinvestment across the mid-cap asset class, evidenced by the fewer institutional strategies focusing on this asset class, according to data from eVestments. Fewer large institutions allocating explicitly to this asset class means less efficient pricing, thus leaving more room for active mid-cap managers to uncover dislocations between fundamentals and price. That’s a key reason THB Asset Management likes opportunity set and potential of mid-cap stocks.