Equities: Passing the baton

Christopher Cuesta, CFA & Manish Maheshwari, CFA 18-Dec-2024

For quite some time domestic large-cap stocks—and the mega caps to be more specific—have been leading the equity market higher. Their earnings, popularity, and subsequent market capitalization growth have been nothing short of astonishing. Yet such success might also be creating unbalanced equity portfolios for many investors. For any investors rebalancing or simply allocating new money to equities, is now a good time to look more closely at the cohort of small, opportunistic companies and rotate down the cap spectrum? We have some thoughts.

Political Change Fuels Opportunity

After a long and sometimes-rancorous election season, we have a clear change of leadership in Washington. Republicans gained control of the White House and Senate, while maintaining a majority in the House of Representatives. The single-party sweep of these three governing bodies was not widely expected, but it now appears to pave the way for the swift introduction of many new initiatives and policies. Combined with current attractive market conditions, this may usher in a new era for U.S. small caps.

The initial market reaction of the election was clear, with equities rallying in anticipation of a lighter regulatory regime, the possibility of lower tax rates, and what is widely considered to be a pro-business and “America-first” environment. Nowhere was this more evident than in the Russell 2000® Index, the primary benchmark for small caps, which has outpaced the S&P 500® and other large-caps indexes in the first month following the election. It seems that investors are sensing that small, nimble and opportunistic domestic companies may be the largest beneficiaries of the pending policy changes and a continuing strong U.S. economic backdrop.

Three Reasons for Small Cap Optimism

Although small cap stocks have rallied since the election, we don’t think it’s too late to consider an allocation. In fact, there are many reasons to believe that this is the beginning of a larger shift in leadership. Here are a few that shape our views.

- Lower Taxes: The President Elect has proposed plans to lower corporate tax rates from 21 to 15% for companies that manufacture in America. By our estimation, U.S. small caps receive approximately 80 to 90% of their revenue domestically. To us, this makes them more appealing relative to large caps, which have higher levels of international revenue and global operational exposure. Small caps seem poised to realize a meaningful increase in earnings and cash flows from lower tax rates, certainly relative to larger companies.

- Deregulation: During his first term, President Elect Trump pledged to remove two existing regulations for each new regulation implemented. We believe that this general concept may be reintroduced. In addition, the Supreme Court overturned the “Chevron Doctrine” this past summer, which was a landmark decision that will facilitate and even encourage companies to challenge prior Federal regulations that may have been hampering growth. If smaller companies will have fewer costs associated with navigating a less-onerous regulatory environment, their earnings outlook should improve.

- Tariffs: One question that many investors have with regard to new economic policies revolves around tariffs and their ultimate impact. If executed strategically, however, the planned imposition of import tariffs may favor domestically focused U.S. small caps, which in theory will be able to better compete against foreign companies that have lower labor and other costs. Larger multinational companies and those who outsource are at the greatest risk for any adverse consequences to new tariffs, which could also potentially increase levels of reshoring. This may provide yet another tailwind to benefit smaller U.S. manufacturers.

In the Early Innings?

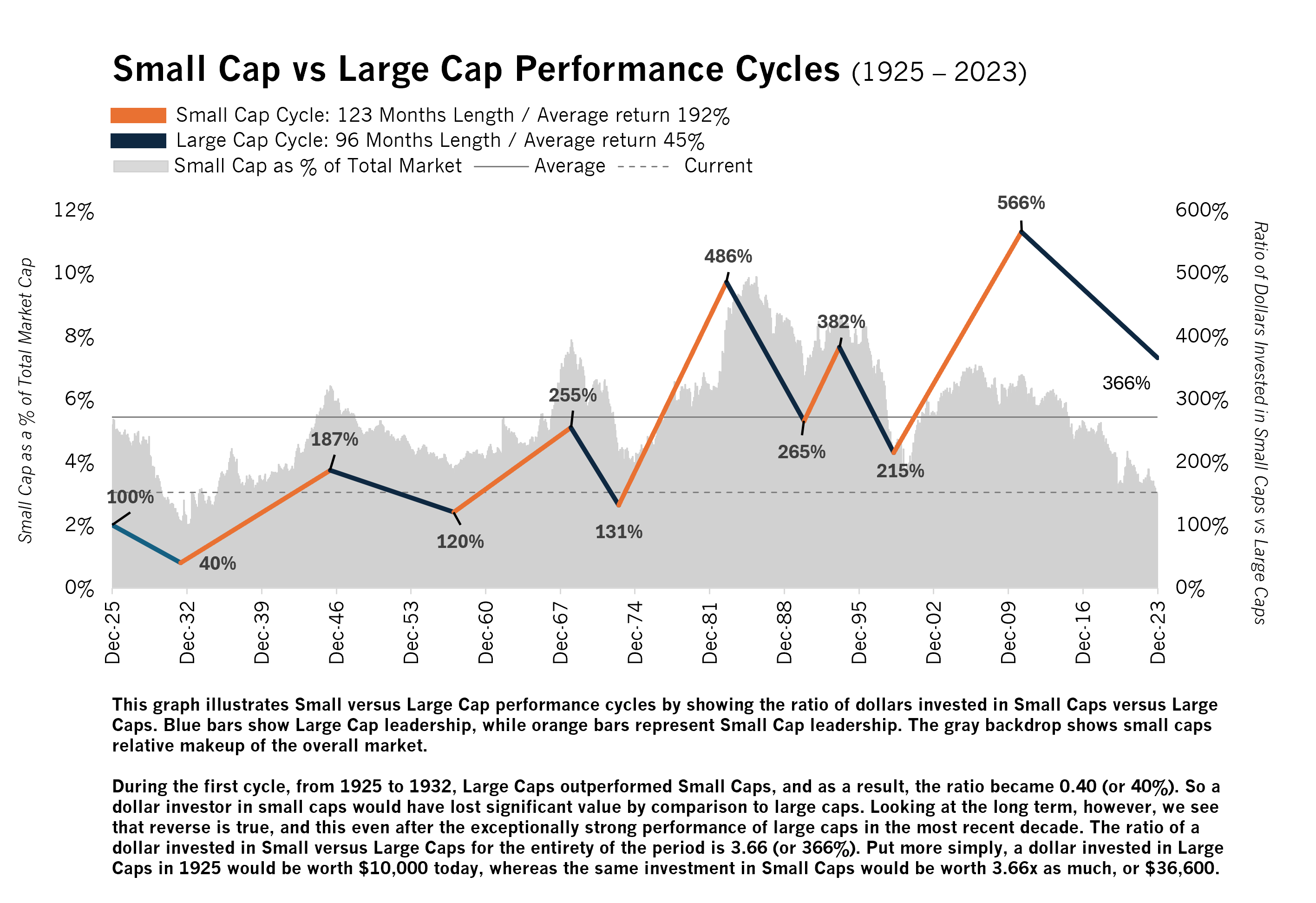

The anticipation of new economic policies that are likely to be implemented beginning in January have clearly fueled optimism for U.S.-based smaller companies. We have already seen the start of what we believe is a long-overdue intra-market rotation away from mega- and large-cap equities into smaller caps. However, a look back at history suggests that we may be in the early innings of a larger move.

Source: Center for Research in Security Prices (CRSP), THB Asset Management

As the chart above illustrates, market leadership by capitalization tends to run in cycles, often relatively long ones. Moreover, our tenure and experience focusing on smaller U.S. companies has given us unique insight into how a broader swath of American entrepreneurs view the U.S. economy and political landscape. In various post-election conversations with management teams, there is undoubtably increased optimism about a pro-growth, less regulated business climate. Plus, we expect merger and acquisition activity to increase as companies look to deploy excess cash flow and small U.S. companies become increasingly attractive from a taxation and growth perspective. And finally, the valuations of smaller stocks look attractive to us relative to large caps.

Of course, we must balance our optimism against the ever-present risks, including the possibility of higher interest rates or the emergence of unforeseen geopolitical issues, among others. On the whole, however, we believe that domestic smaller-cap stocks are well positioned and have the potential to assume the mantle of equity market leadership in 2025 and beyond.