Equities: Passively ignoring risks?

WestEnd Advisors Investment Team 11-Mar-2025

The S&P 500®, a widely used proxy for U.S. equities, is coming off back-to-back years of 20-plus percent returns. This is an index that many passive funds seek to track in their domestic core equity portfolios. Given the recent strong performance, it’s easy to see why some investors gravitate to this approach. However, many investors may be underestimating—or perhaps ignoring—the risks embedded in their passive core equity funds. Upon closer inspection, is there a better way to build a core equity allocation?

Broad Appeal, Concentrated Risk?

Put simply, passive investing seeks to deliver broad, market-like returns (before fees and expenses), and in turn accepts the volatility and risks embedded in the broad market. On the surface, it seems like a simple proposition, and it is easy to see the appeal of a “set it and forget it” passive approach when the market is moving broadly higher. Further, many investors may be drawn to the relatively low fees involved in passive investing. Others may view active investing as futile in highly liquid areas of the market like U.S. large-cap equities, which could be seen as too informationally efficient for bottom-up stock picking to consistently generate excess return. While such arguments may have merit, we believe they fail to address key risks inherent in a passive approach and overlook ways in which active management can both help mitigate risk and potentially achieve excess returns.

A look at how the indices that underpin passive investing are constructed can illuminate certain risks of passive investing. Like most major stock indices, the S&P 500 is a market-cap-weighted index, whereby the weights of constituents are based on their market capitalization, or size. Given that some of the largest companies in the index have outperformed in recent years, and thus their weights in the index have increased, the performance of the S&P 500 has become deeply reliant on just a handful of stocks. At the end of 2024, the top 10 stocks (just 2% of constituents) made up over 37% of the index. This calls into question how well a fund based on this index is diversifying away stock-specific risk. At a higher level, where companies with similar economic activities (and often highly correlated stock performance) are grouped into eleven sectors, market concentration is even more dramatic. The largest three sectors in the S&P 500 represented a combined weight of over 57% of the index at the end of 2024. Further, three sectors that are dominated by the AI and technology-related companies that comprise the so-called “Magnificent 7” also collectively made up over half of the index.

A simple way to understand this concentration risk is that passive investment in market cap-weighted equity indices is inherently backward-looking. Those areas that have grown the most in the past have the largest weights, which can leave passive portfolios concentrated in areas with elevated valuations or whose economic tailwinds may be long in the tooth. At the same time, these indexed passive funds may have limited exposure to areas of the market that have underperformed but may be poised to excel as economic conditions evolve.

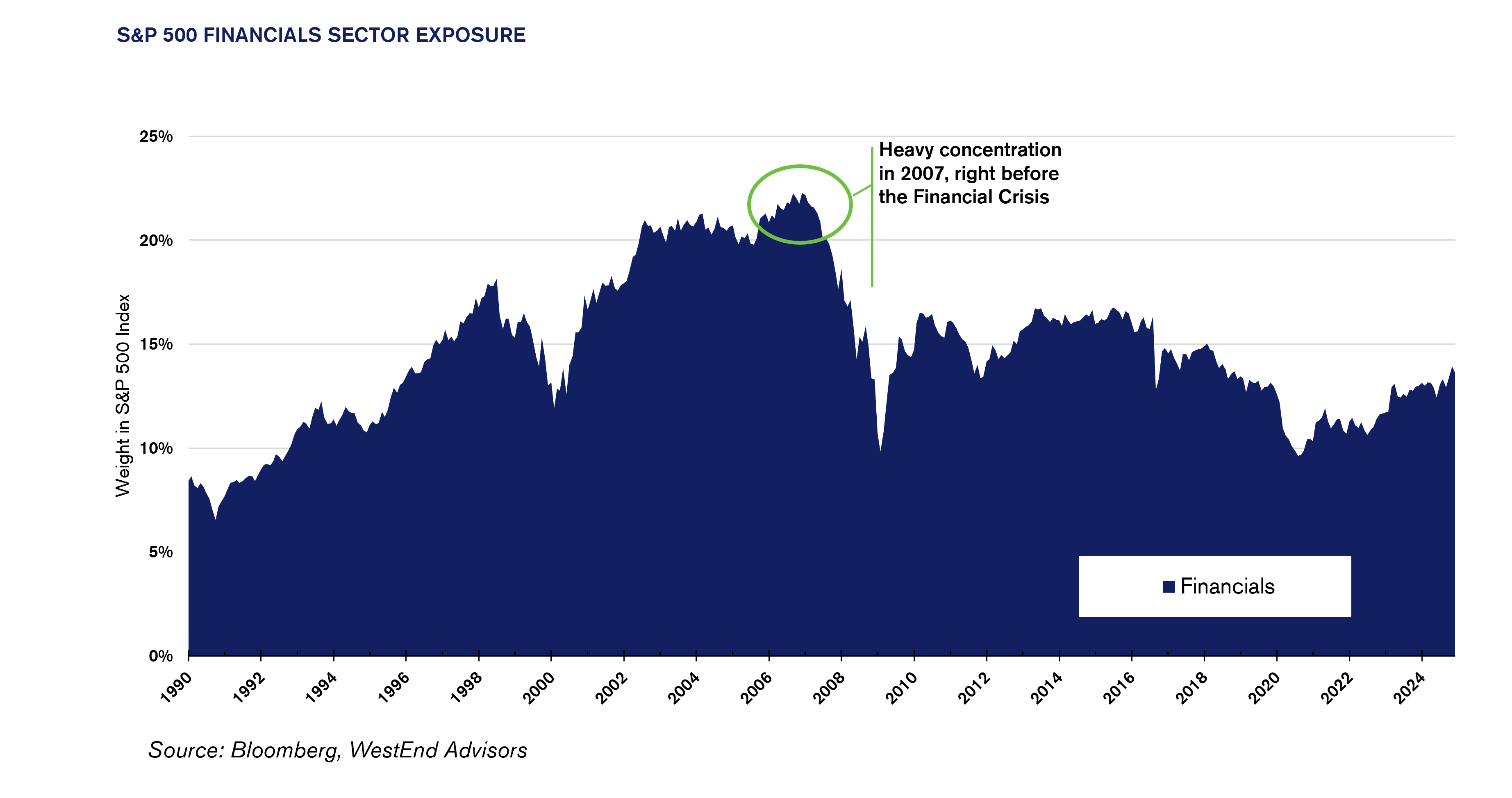

One example of backward-looking index construction leading to concentration risk was the rise and fall of the Financials sector around the Global Financial Crisis of 2008. In the early 2000s, as other areas of the economy struggled in the aftermath of the Dot-Com Bubble and subsequent recession, Financials stocks rode a wave of housing investment and financial engineering to regularly outperform the S&P 500. By the start of 2007, there was a historically large concentration of financial services companies in the S&P 500, accounting for more than 20 percent of the index just as the Global Financial Crisis hit. Passive investors had no way to adjust for that that risk. Rather, their portfolios were bloated with many of the companies hit hardest by the crisis.

Time and again, the market-cap structured portfolios based on the S&P 500 seem to have been built by looking in the rear-view mirror. Often, they have been overexposed or underexposed to certain sectors of the market at the wrong time. Other examples include the low exposure to technology in the mid-1990s as the tech boom gained steam, and the subsequent over-exposure to Information Technology companies at the peak of the dot-com bubble in 2001.

Fast forward to today and one might be wondering if history is repeating (or at least rhyming). The Information Technology and Communication Services sectors have ballooned to represent over 40% of the S&P 500, as of early 2025, which is reminiscent of the peak of the 1990s tech bubble. Is this really what investors want to passively accept in their core equity allocation today?

A Different Approach

Fortunately, investors do not need to be subjected to the whims and unwanted ramifications of passive, cap-weighted portfolios. We believe that a top-down, macroeconomically driven approach to dynamic sector allocation and avoidance is a better way to build a core equity position. Shifting sector allocations opportunistically (and ideally slightly ahead of the cycle) based on macroeconomic analysis, WestEnd Advisors seeks to manage risk and offer the potential for outperformance of active management without relying on the questionable efficacy of stock picking.

So what does that mean for today? As of February 2025, we continue to see the U.S. economy in a late-cycle environment. The economy has been resilient, and while various macroeconomic tailwinds are fading, we expect GDP should continue to grow thanks, in part, to consumer spending buoyed by personal income growth and accumulated household wealth. Moreover, lower inflation could provide the Fed with continued flexibility, particularly in response to further labor market softening. However, upside risks to inflation are more prevalent than a year ago, and some policy wildcards, such as tariffs, could also have an impact.

At the sector level, we expect leadership could continue to broaden out, and we see a range of opportunities and risks. The tech-related sectors that were boosted by enthusiasm for AI in 2024 carry some of the highest sector valuations, even after bouts of volatility so far this year. While these sectors have begun to see some positive revenue impact from AI, we are mindful of the risk of disappointing elevated investor expectations in 2025. As such, we are currently underweight U.S. Information Technology across portfolios and have tilted our Technology exposure toward the software industry, which we believe carries more palatable valuations alongside of consistent growth.

We believe the U.S. Financials should benefit from continued (if moderate) rate cuts resulting in a steeper yield curve, as well as a continued resurgence of capital markets activity. At the same time, we are avoiding other economically cyclical sectors, like Industrials and Materials, as well as the highly interest rate sensitive Real Estate and Utilities sectors in the U.S. While we have also reduced defensive exposure as recession risk has diminished, in our view, we believe the stable earnings growth potential of the defensive U.S. Health Care and Consumer Staples sectors remains attractive, given ongoing late-cycle economic risks.

This ability to dynamically align portfolios with our macroeconomic outlook is preferable, in our view, to passively accepting the backward-looking exposures offered by cap-weighted index funds. All too often investors may be ignoring some of the unintended risks and consequences of passive investing. We believe positioning at the core of an investor’s portfolio should not be simply left to what did well before, which calls to mind perhaps the most crucial disclaimer in investing: “Past performance is no guarantee of future performance.”

This report should not be relied upon as investment advice or recommendations and is not intended to predict the performance of any investment. The information contained herein is not intended to be an offer to provide investment advisory services. Such an offer may only be made if accompanied by WestEnd Advisors’ SEC Form ADV Part 2. These opinions may change at any time without prior notice. All investments carry a certain degree of risk including the possible loss of principal, and an investment should be made with an understanding of the risks involved with owning a particular security or asset class. Portfolio characteristics and/or allocations are generally averages and are for illustrative purposes only and do not reflect the investments of an actual portfolio unless otherwise noted. Portfolios that are concentrated in a specific sector or industry may be subject to a higher degree of market risk than a portfolio whose investments are more diversified. While every effort has been made to verify the information contained herein, we make no representation as to its accuracy.