Equities: Positioning for a rebound?

Brian Jacobs, CFA 20-Jun-2023

The changing interest rate regime certainly did a number on growth stocks and, in particular, small-cap growth. As the market began pricing in higher interest rates and the Federal Reserve embarked on its historic efforts to combat inflation, investors seemingly eschewed smaller growth-oriented stocks at all costs.

Nevertheless, our team believes that despite the multi-year underperformance of small fast-growing companies (especially the highest growth segment of this category), small growth stocks are well positioned over the secular horizon. In our view, we are still in the early stages of a secular shift that is altering how consumers, businesses and employees interact. This shift began during the early days of the pandemic, which in effect was a massive “test run” of technology-aided solutions. These technologies are constantly being refined, and new tools such as artificial intelligence are also poised to make a material impact in the performance of the small growth asset class in coming years.

Below are three reasons—and three graphs—that articulate why we believe that small cap growth presents an attractive opportunity for fundamental-based, valuation-focused, contrarian investors. Moreover, if the Fed is truly set to pause its rate hikes as many suggest, the recent headwinds could shift to tailwinds. This only strengthens our conviction in this sector.

The Backdrop

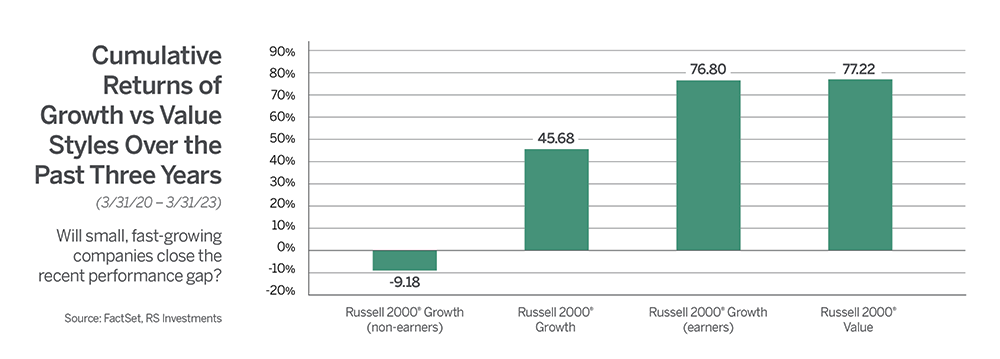

Small-cap growth stocks have endured a period of punishment. As the cost of capital increased, speculative companies without current earnings sold off sharply. This included special purpose acquisition companies (SPACs), often referred to as blank check companies, as well as meme stocks that were pushed to unthinkable valuations in the early stages of the Covid stimulus-infused melt-up. That’s understandable. Yet even fast-growing small-cap companies with solid fundamentals and intriguing long-term potential have been punished. This has primarily affected companies with higher growth trajectories and valuations, particularly in technology and biotechnology sectors where the real business opportunity isn’t a few months or quarters, but often years away.

The graph below illustrates the astonishing disparity between the performance of small-cap growth and small-cap value over the past few years.

The Opportunity

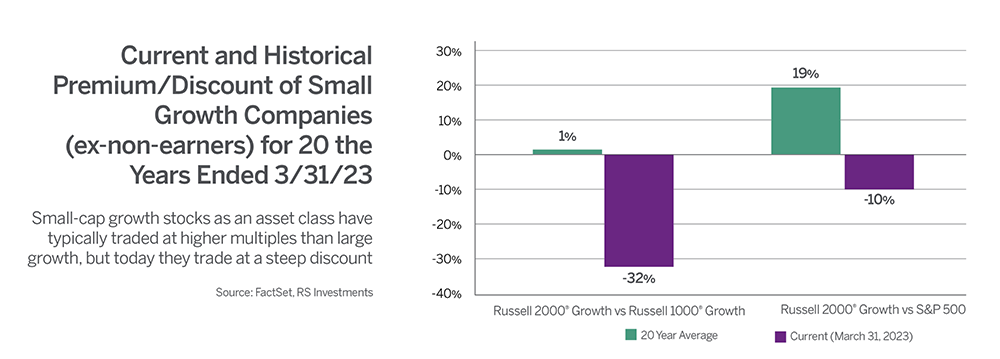

The divergence in recent performance does not shake our conviction in small, high-growth companies with strong prospective fundamentals. In fact, it merely strengthens our belief given that many such companies now trade at historically low valuations compared to other areas of the growth market. According to our analysis of data pulled from Factset, the forward P/E ratio of the Russell 2000 Growth Index (excluding non-earners) stands at a modest 16.2x, a discount of more than 30% to larger growth stocks in the Russell 1000 Growth Index, and even cheaper than the average of S&P 500 companies (which also have materially slower growth forecasts). These are both levels never experienced in the 40-plus years since inception of the Russell indices in 1979, and it may signal an opportunity to find fast-growing companies at reasonable valuations, in our team’s opinion.

The Outlook

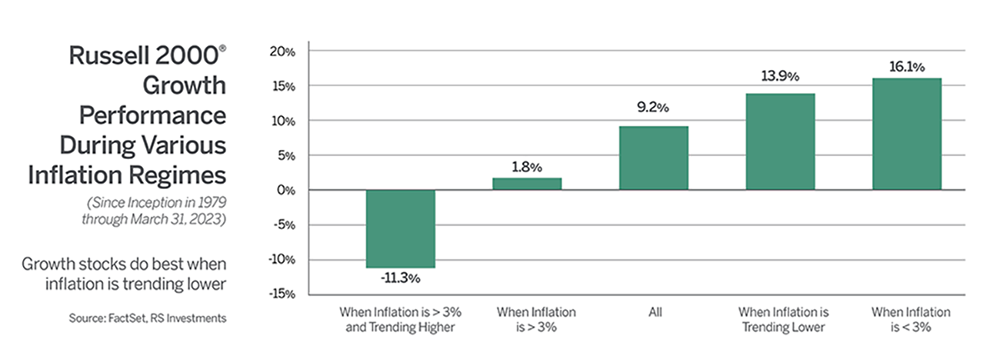

In addition to attractive valuations, we believe that the economic backdrop has shifted favorably in recent months. After a period of rapid rate tightening, the Fed has signaled they may be approaching the end of this rate-hike cycle as inflation appears to have peaked. The Consumer Price Index increased 4.9% year-over-year in April, according to the U.S. Bureau of Labor Statistics, but this is well off its high reading of 9.1% in June 2022. And based on our analysis of historical data, we find that small growth stocks perform well when inflation is trending lower, especially when retreating from higher-than-normal levels. This is illustrated in the graph below and may signal a promising environment for small-cap growth stocks.

If inflation and interest rates recede, we believe that small-cap growth stocks may once again exhibit signs of strength. Thus, the convergence of historically low valuations, robust growth prospects, and a supportive macroeconomic environment suggests a promising future for small-cap growth stocks. It may not be a popular opinion at this time, but that never bothers contrarians. Investors and their advisors might want to revisit how small-cap growth stocks may fit strategically into a broader, well diversified equity portfolio.