Equities: The Growth-Value Divide

Brian Jacobs, CFA 20-Oct-2022

With the exception of commodities and utilities, equity investors have not been high-fiving much this year. Through the first three quarters of 2022, it’s been a competition between which sectors and styles are doing less bad. Small-cap growth, in particular, has substantially underperformed its small value counterpart to date this year. Yet this very fact should pique the interest of contrarian investors, and it makes a compelling case for any new, long-term equity allocations.

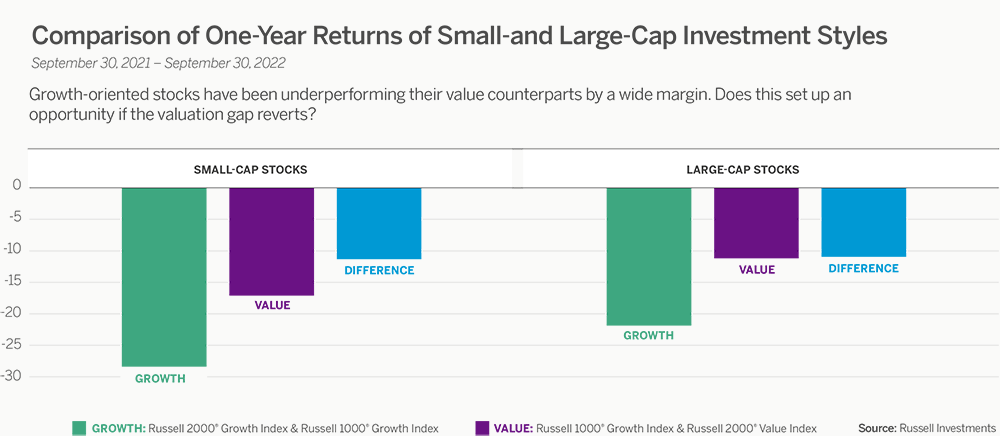

The graph below illustrates the cumulative performance of small- and large-cap growth versus their value style counterparts for the past year. It might be shocking to see just how wide the dispersion has been irrespective of fundamentals or long-term potential of many small and fast-growing companies.

Getting more granular on performance within the indexes, our research and analysis suggests that the underperformance of the small-growth investment style (as measured by Russell 2000 Growth Index) has been largely concentrated in those companies with higher growth trajectories and higher valuations. In contrast, stocks that were the cheapest (and often the less-intriguing growth stories) within the Russell 2000 Growth Index actually held up relatively well, especially compared to the much better-performing small value universe (as measured by Russell 2000 Value Index). Yet it’s important to remember that investors who allocate to the small growth style often do so as a means to add a potential return enhancer to their portfolio by capturing those dynamic companies with greatest long-term earnings potential, including biotechnology companies with developmental drugs in the pipeline. These and other growth-oriented companies (many without present day earnings) have been absolutely punished in the current environment.

The near-term divergence illustrated above does nothing to dispel our long-held belief in an allocation to small, high-growth companies with strong fundamentals. If anything, our conviction is stronger given that many such companies may be trading at cheap, multi-decade low valuations. In fact, as of the end of the third quarter 2022, the Russell 2000 Growth Index traded at a forward P/E of just 13.0x (excluding those non-earners), levels that are at or near the lows we saw during the 2008/09 global financial crisis and 2020 pandemic lows.

Does this spell opportunity? Perhaps. At some point we believe that we will see a reversion to the mean, whereby the Grand Canyon-sized valuation gap between small growth and small value styles shrinks to historical levels (and maybe less). Nobody knows precisely when the sectors that are traditionally more value-oriented, such as energy, materials & processing, and producer durables, will cede their leadership position as the better performing areas of the market. Shifts in sentiment (and sector rotations) tend to happen when investors expect it least. And when these companies stop being punished and once again start being valued based on their fundamentals and long-term potential, we believe that small growth as an investment style should have a long runway just to get back to mean historical valuations.