Floating rate: A life raft for bond investors?

JAMES TRACY 08-Mar-2021

Fixed income investors seeking higher yield potential have an array of choices. Yet floating-rate bank loans are unique—they are among the few fixed income asset classes that have the potential to maintain or increase in value in a rising rate environment. Why? The interest rate on floating rate loans resets every 90 days based on a short-term interest rate benchmark, the three-month London Interbank Offered Rate (LIBOR). This important feature should not be overlooked at a time when some investors are seeking both higher yields and protection against the possibility of rising interest rates.

Why are investors talking about this nuanced area of the fixed income world? To put it bluntly, some are worried. Think about the current environment. On one hand, the current low rates make it difficult to capture adequate income. As of late-February, the 10-Year Treasury was yielding just 1.4% (and that was after a move higher). That’s just not going to cut it for many investors.

On the other hand, inflation is a growing concern. Over the past year, the Federal Reserve and Congress provided massive fiscal and monetary medicine to revive the economy and stabilize financial markets. But there are possible side-effects, and many investors are now wondering whether we are on the cusp of a new era of inflation—maybe not this quarter or next, but soon.

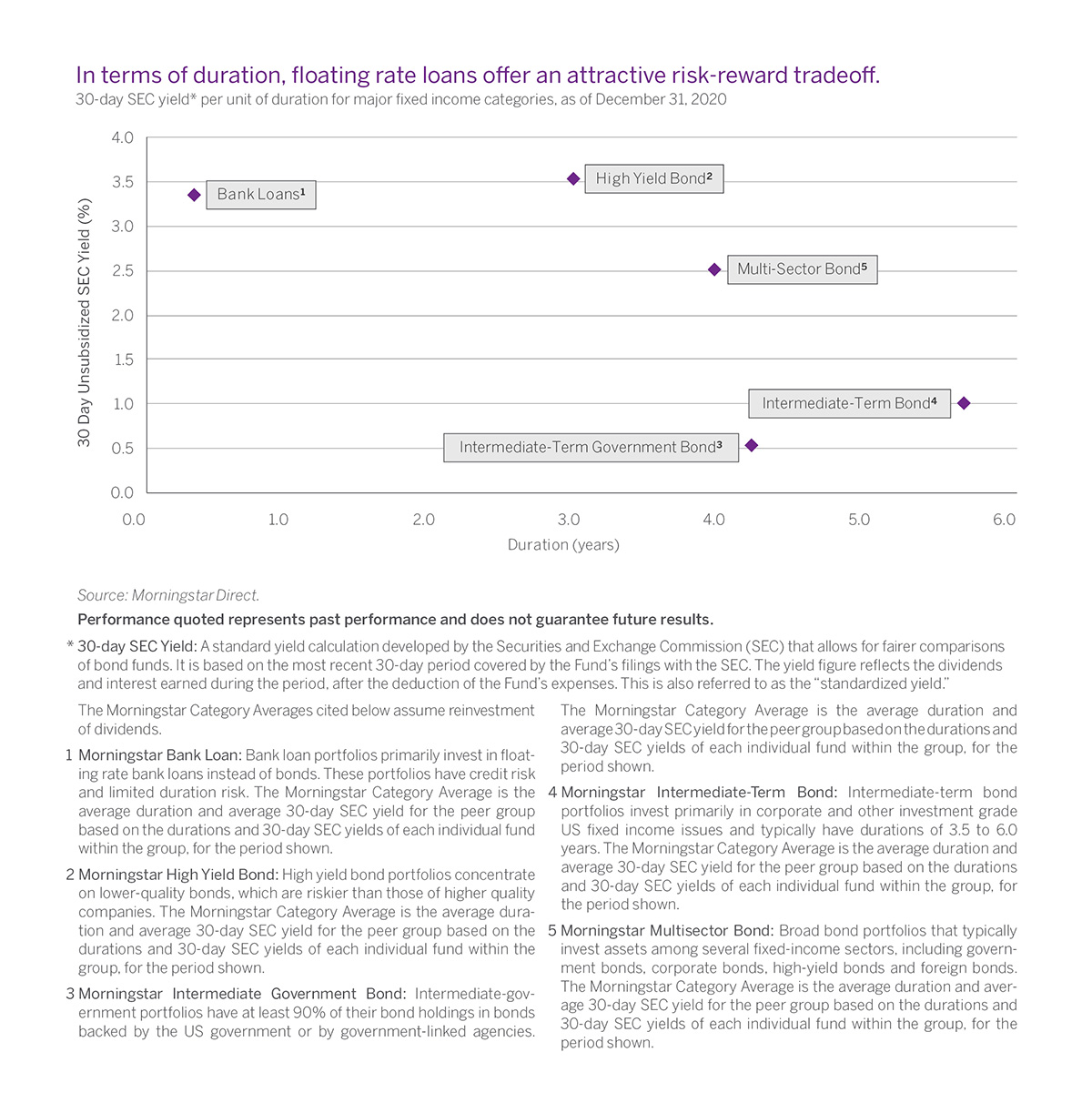

Bond analysts often use duration—a favored metric of interest rate sensitivity—as a means to evaluate bond portfolios and gauge how they might perform a rising rate environment or in the event that a new inflationary regime emerges.

Of all the major fixed income asset classes, floating-rate loans, represented by the Morningstar Bank Loan category on the accompanying chart, seemingly offered the best combination of attractive yield and low interest rate risk as of year end 2020.

Of course, investors should always be aware of other risks with floating rate bank loans, including credit and liquidity. But this is exactly why fundamental credit analysis and sector selection—hallmarks of active management—are so important in the floating rate bank loan segment, as compared to a passive approach whereby such decisions are based on an index and there is no chance to tilt or fine-tune the portfolio.

Of course, investors should always be aware of other risks with floating rate bank loans, including credit and liquidity. But this is exactly why fundamental credit analysis and sector selection—hallmarks of active management—are so important in the floating rate bank loan segment, as compared to a passive approach whereby such decisions are based on an index and there is no chance to tilt or fine-tune the portfolio.

Given the current backdrop and their low duration, floating rate bank loans just might be worth a second look.