Growth investing: don't jump to conclusions

BRIAN JACOBS, CFA 27-Apr-2021

The specter of rising interest rates has been a hot topic among fixed income investors. But the matter has been on the minds of growth investors as well. Should they be concerned about rising interest rates, or is conventional wisdom that rising rates hurt growth stocks—and small-cap growth in particular—more fiction than fact?

Rather than rely on old Wall Street platitudes, we decided to look at the evidence. Good news: history suggests that small-cap growth investors need not be so anxious in the face of rising rates. In fact, it appears that smaller, fast-moving companies may actually be able to press their advantages, further improving the likelihood of outperformance should we enter a prolonged rising-rate environment.

.jpg)

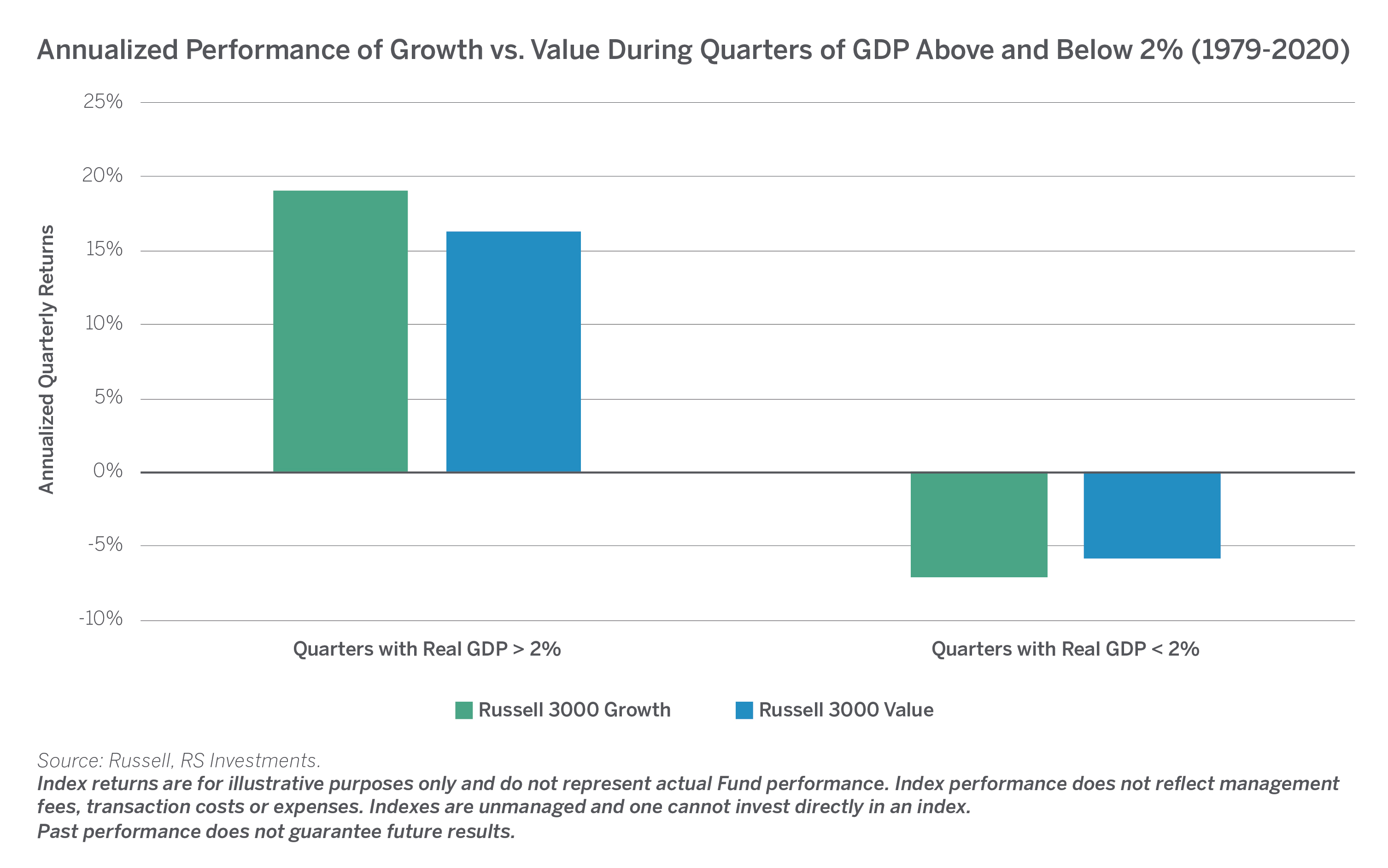

After looking back at various periods of rising interest rates over the past 25 years, our thesis was confirmed by the strong absolute performance for the growth stock asset class, and the especially strong relative performance of smaller growth-oriented stocks versus their value-oriented counterparts. Although we acknowledge that a rising rate environment—thanks mostly to improving economic conditions—can provide a tailwind to all types equities, the outperformance of growth and small growth investing styles during these periods is evidenced in the chart above

Perhaps what will be most surprising is that certain equity indexes, such as the S&P 500 Low Volatility Indexi and the S&P 500 High Dividend Indexii, which are typically viewed as lower risk, have lagged during these same periods. We believe that the relative outperformance of smaller growth-oriented stocks during rising rate periods can be attributed in part by the strong relationship between economic growth and interest rates. Interest rates tend to rise when economic conditions are viewed as improving, which should allow smaller, growth-oriented companies to continue growing earnings despite higher interest rates. Moreover, earnings growth may cushion any impact that a higher discount rate may have on borrowing costs and future earnings.

So how does all this translate today? When rates head higher—already having moved sharply during the first quarter of 2021—dynamic growth strategies may shine. In terms of valuations, growth stocks are no longer the extreme bargain they were back during the depths of the pandemic in mid-2020. But that doesn’t mean there’s no value in growth today. To the contrary. The economic outlook appears to be improving, and thus we believe there is a long runway for potential earnings growth. This positive outlook is based on:

1. The pandemic, in our opinion, accelerated a massive “test-run” of technology-aided solutions and helped people work, shop, and communicate from home. This should speed up the adoption of various new technologies at the expense of legacy products and services.

2. We see an ongoing shift in sentiment among consumers, businesses and investors as the economy returns to a more normal state and pent-up demand is unleashed.

3. The unprecedented fiscal and monetary stimulus, which is putting money directly into the hands of consumers and businesses, is not only helping maintain market order, but it’s also allowing pockets of the economy to bounce back more quickly.

Finally, the Federal Reserve has been increasing its forecast for real GDP growth and now is projecting 6.5% growth for the 2021 and 3.3% growth for 2022. A number of value-oriented industries already have bounced materially, while many growth companies—even those with attractive fundamentals—have lagged in the rebound. This creates opportunity. The economy is looking up, and we feel the near-term represents a period in which innovative companies are poised to re-emerge as market leaders despite the interest rate forecast.

i The S&P500 Low Volatility Index measures the performance of the 100 least volatile stocks in the S&P 500® based on their historical volatility. The index is designed to serve as a benchmark for low volatility investing in the US stock market.

ii The S&P 500 High Dividend Index consists of 80 high dividend-yielding companies within the S&P 500 (the “Index Universe”). Constituents are equal weighted.