High-yield: Riding out a rough period

JULIANNE BASS, CFA 09-Sep-2019

High-yield bonds have tossed around in recent months, largely due to the same related factors behind the volatility flare-up in the stock market: a slowing global economy and the downside impacts of the U.S.-China trade dispute that many fear may get still worse.

That high-yield and equities would share a rough ride isn’t a surprise, given that both are risk assets correlated to corporate fundamentals. Within high-yield, the roughest ride has been in the riskiest segment – bonds rated CCC or below.

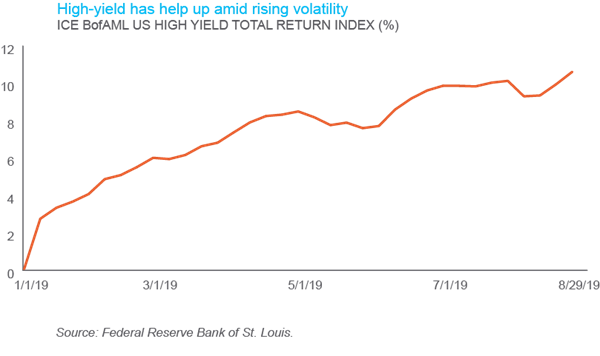

But while the mood around high-yield may be more on edge, performance is holding up – for 2019, the ICE BofAML U.S. High Yield Total Return Index had gained around 11% as of late August. Bonds rated BB have been the key performance driver as investors sought to reduce portfolio risk.

Yield spreads relative to investment-grade corporates have also been volatile lately.

The yield gap between BBB and BB – where investment-grade and high-yield meet – began August at 70 basis points (0.7%), but in a matter of few days blew out to 125 bp after President Trump announced another yet round of tariffs aimed at China. Even with trade tensions persisting, BBB-to-BB spreads have narrowed to under 75 bp.

Within high-yield’s rating tiers, however, spreads have widened – the yield difference between BB and CCC has expanded by nearly a percentage point in August. This suggests growing market worries about the economy following the Federal Reserve’s late-July interest rate cut. If the pessimism proves overdone, an opportunity could present itself should spreads within high-yield start to tighten again.

Offering a short-term outlook for high-yield is difficult, perhaps even futile, in this uncertain environment. Our case for a strategic allocation to high-yield, however, is straightforward:

YIELD PICKUP: Over time, the income generated by a bond accounts for the lion’s share of its total return. Yield is hard to come by in this prolonged period of stubbornly low interest rates – this positions the high-yield segment as a valuable source of risk-adjusted income relative to other fixed-income offerings.

RELATIVE RISK: The high-yield sector shares a number of key qualities with equities – the result is a positive performance correlation. On a risk/return basis, the high-yield index has over time captured most of the upside offered by the S&P 500, but with much less volatility (measured by standard deviation).

DIVERSIFICATION: High-yield is a component of the fixed-income market, but it carries a low correlation to the higher-rated bonds that typically form core portfolio holdings – the long-term correlation to Treasuries is actually negative. While high-yield comes with more credit risk than other bonds, the sector tends to be less sensitive to changing interest rates.