Let it go

SCOTT NEEB 15-Aug-2018

Some of the most successful retirement plan advisors choose to outsource some of their responsibilities to independent third-party providers and partners.

It’s not about avoiding work. Actually, the reasoning is quite sound: partnering with other experts allows plan advisors to put time back in their day so they can focus on business development and client servicing.

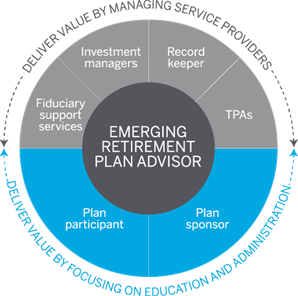

For instance, this graphic depicts a structure that leaves administration and education in the capable hands of the advisor and then relies on experts for the following duties:

fiduciary support services, investment management, and record keeping.

Deliver value by managing service providers

Retirement plan advisors can be extremely valuable to a plan sponsor by guiding them toward the best decisions. For example:

Educate plan sponsors on various service providers, assessing:

- What they offer

- What their strengths and weaknesses are

- Their pricing and fees

- Assist with service provider selection

- Assist with plan conversion and any change in service providers

If you are onboarding a new plan sponsor, bear in mind that the path of least resistance is to not change the vendor, unless it is in the best interest of the plan and its participants. In most instances, when something is wrong, it isn’t because the plan is broken. It is usually because the previous advisor wasn’t doing his or her job.

When you take over a new plan, get the plan sponsor to divulge his or her biggest gripe and address it.

In fact, these questions can help you figure out what the plan sponsor wants to fix:

- If you could start again from scratch, what three areas would you want to improve upon the most?

- What three issues worry you the most today?

- What three things influence building trust with service providers? (Prompted answers could include: Delivering on promises, making things simple for participants, calling me regularly.)

- What services are most important to you? (Prompted answers could include: Monitoring and reviewing investment options, employee education and enrollment meetings, plan design, fee transparency.)

There is no doubt that plan sponsors and participants need help. As a retirement plan advisor you have a tremendous opportunity to stand apart by focusing on servicing your clients through general investment education, rather than picking investments.