Microcaps: Private equity doppelganger?

CHRISTOPHER CUESTA, CFA MANISH MAHESHWARI, CFA 05-Jun-2022

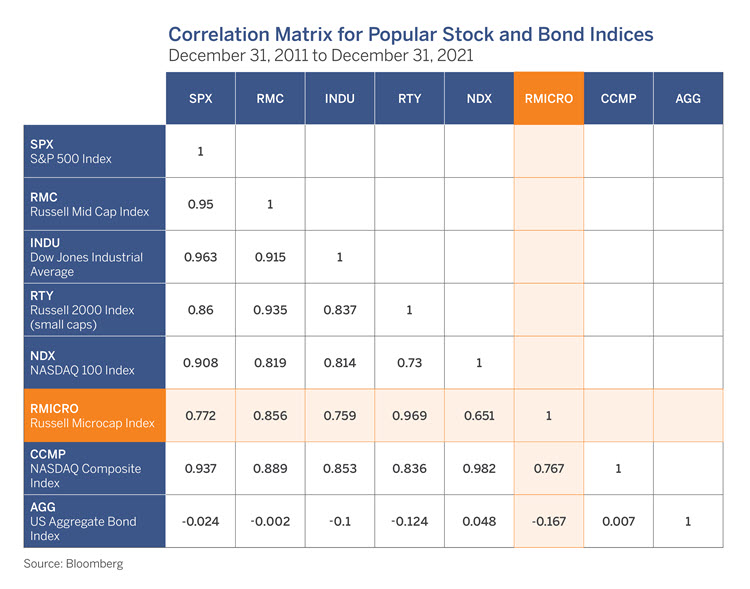

When a rising tide lifts all boats, nobody seems to mind. But when volatility returns to financial markets and price action goes south, investors are reminded of the true value of diversification. Herein lies one potential advantage of micro-cap equities. These small and oft-overlooked publicly traded companies (typically with a market capitalization between $30 million and $1 billion) have shown lower pair-wise correlation to other major asset classes over the long term.

To date this year, we’ve witnessed both stocks and bonds selling off, providing a stark reminder as to why investors—both retail and institutional—allocate to alternative asset classes that offer the promise of long-term return enhancement with low correlations to other parts of the portfolio. Incidentally, this is also one of the key arguments for why investors allocate to private equity (simply defined as that category of companies not publicly traded and not listed on a stock exchange).

Private equity returns, while still somewhat dependent on the underlying macro backdrop, are not subject to the vagaries of near-term public market sentiment, which can be mercurial and change quickly. Plus, there is no daily price discovery, nor is there pressure to manage to analysts’ quarterly earnings expectations. Private equity is for investors playing the long game. In theory, this allows private companies more latitude in maintaining a longer-term focus and executing successful growth strategies.

So what’s the connection here? We believe that the micro-cap equities offer many similarities to private equity investments. Thus, the micro-cap niche provides investors a unique opportunity to mine the potential benefits of private equity, but without the typical high-fee structure, high minimum investments, or liquidity restrictions typical to most private equity strategies.

These two asset types—private equity and micro-cap public equities—have many commonalities, both in terms of how they might generate similar returns and how they might function within a broadly diversified investment portfolio. In our experience, we believe that company size (as defined by market capitalization or deal value), insider or founder ownership, domestic focus, a large investable universe, and inherent inefficiencies within these businesses are all common characteristics that micro-cap listed companies share with certain private equity.

Moreover, smaller niche businesses are often attractive acquisition candidates. And in some cases if they are well-capitalized, these small companies may have an opportunity to make acquisitions themselves in order to enter new verticals, complete an existing product suite, or consolidate market share. This is part of a typical playbook associated with private equity. It’s also reasonable to expect that an increasing flow of money to private equity in recent years may lead to increased acquisition activity among micro-cap companies. This could, in theory, provide another tailwind to forward return expectations.

All this suggests that actively managed micro-cap strategies—depending on the investment philosophy of the individual manager—might be used as a reasonable surrogate by both investors and institutions looking to add to their private equity allocation. In a time when portfolio construction is under scrutiny and alternative asset classes are being valued for their lower correlations and return potential, investors may come to realize that micro-cap equities just might have a larger role in a diversified portfolio.