No cash, no problem

MIKE REYNAL 15-Aug-2018

I recently visited China and snapped this picture. In case your Mandarin is rusty, it translates loosely to: Cash not accepted.

It's a simple statement, but with surprisingly complex and far-reaching ramifications. These signs are widespread across the country—and third-party online payment solution Alipay is ubiquitous—in stores, restaurants, train stations, and seemingly everywhere. In China, mobile payment is the standard across all ages and socioeconomic levels. An article in The Wall Street Journal from earlier this year even pointed out that some panhandlers use mobile payment apps as a means to make “donations” easier.

Why should you care? For starters, it’s a stark reminder that emerging markets are not always secondary to developed markets, especially with regard to adopting and implementing new technologies. Parochial Westerners often forget that there’s a whole other world out there where investment and development moves at warp speed. The widespread adoption of mobile payments is but one example of how emerging markets are the real leaders in many aspects of the digital economy.

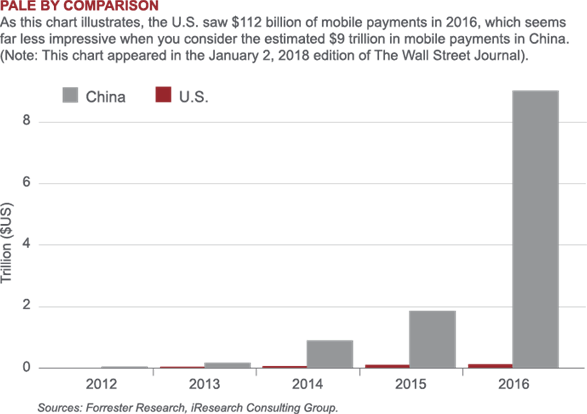

Consider that the U.S. saw $112 billion of mobile payments in 2016, according to estimates from Forrester Research. This may sound substantial, but it pales in comparison to the estimated $9 trillion of mobile payments in China, according to iResearch Consulting Group. The impact of this is enormous, and not just for the fintech and mobile banking players. The rise of digital pay has a ripple effect across countless industries and the entire economy. Already e-commerce penetration is quite large across China, and the march toward a cashless society is providing fuel to business disruptors in ride-hailing, bike-sharing, and beyond.

The use of mobile payments is reshaping how people spend, borrow and even invest. Moreover, in a geographically expansive country like China that is building out its digital infrastructure rapidly, mobile pay apps are also being used to mine an incredible amount of data on consumer spending habits, which can be used as another marketing tool to target the burgeoning consumer class. The long-term ramifications are exciting.

So while many investors are myopically focused on how near-term fluctuations in the U.S. dollar and U.S. Treasury yields might impact next quarters’ results, the eye-popping digital investment in China (and in other emerging markets) continues unabated. A mobile payment infrastructure that is more mature in China than just about any developed market is simply one example that illustrates why we remain constructive on emerging markets for the long term.