Pairs well with...

BRIAN SMITH, CFA 10-Sep-2020

Traditionally, the Bloomberg Barclays Aggregate Index (Agg) has been used as a proxy for the overall bond market—a little like an S&P 500 Index for the fixed income world. Many investors use the Agg as a benchmark to build a diversified fixed income portfolio because it includes a wide swath of securities, including Treasuries, mortgage-backed securities (MBS), asset-backed securities (ABS), and corporate securities, among others.

However, investors who rely on the Agg exclusively to guide their fixed income positioning might be limiting themselves or taking on more risk than they realize. In fact, we believe that adding a healthy allocation of short-term corporate bonds might go a long way to enhance the risk-adjusted return potential of a broader fixed income portfolio, while reducing interest rate risk over the long term.

For starters, the Agg is heavily tilted toward U.S. government securities and MBS. Although this has always been the case, investors might not realize that the Agg has changed over the years and how much the index’s average duration, which is a measure of how sensitive a security is to changes in interest rates, has increased. The average duration of the Agg has gone from just over 4.9 a decade ago to approximately 6.2 at year-end 2020.

In addition, the weighting of corporate bonds within the Agg has increased from approximately 25% at year-end 2019 to 27% as of the second quarter 2020. This reflects the very high level of new corporate issuance during this time and illustrates how trends in corporate finance can potentially alter the risk profile of a portfolio.

One possible strategic, long-term solution to improving the risk/reward profile of a bond portfolio is to include an allocation to short-term bonds, and in particular, corporate short-term bonds. We believe this provides two potential benefits: the ability to capture excess return (versus the risk-free rate, which is very low in this environment) while also lowering duration.¹ Pairing shorter-term corporate bonds with the Agg results in a higher Sharpe ratio² (which is a metric used to measure risk-adjusted returns—higher being better).

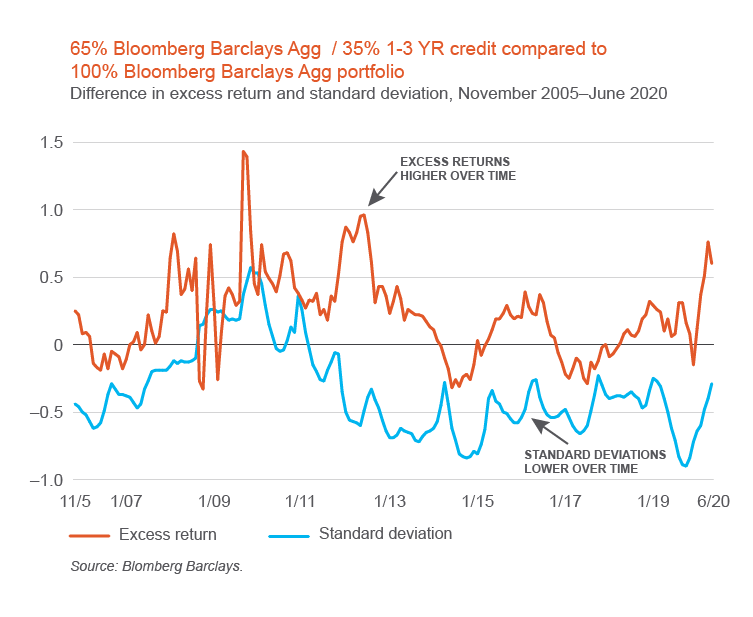

To demonstrate this, we looked back over 20 years and compared a pure Agg portfolio with a more diversified approach (one that pairs a 65% Agg portfolio with 35% short-term corporate bonds, represented by the Bloomberg Barclays U.S. 1-3 Year Credit Index.)

Index returns shown for illustrative purposes only. Indexes do not incur management fees or other expenses; one cannot invest directly in an index.

As the chart demonstrates, short-term corporate bonds appear to pair well with the Agg. The hypothetical blended index portfolio provides a higher excess return over time, along with lower standard deviations. Accordingly, such a portfolio produced superior risk-adjusted returns, as measured by Sharpe ratio.