Small-cap growth: Managing risky business

BRIAN JACOBS, CFA 30-Sep-2019

One of the hardest things about small-cap growth investing is accepting the inherent volatility associated with the asset class. This is not an insignificant challenge, particularly when news flow—often extraneous to a specific business—can roil markets and move stocks. Consider some small-cap realities.

Intra-year drawdowns of small growth stocks—as represented by the Russell 2000® Growth Index, the leading benchmark for small-cap growth managers—are not uncommon, evidenced by periodic pullbacks of 15% or greater in seven of the past dozen years. In addition, small growth stocks have delivered a negative monthly return in more than one-third of all months since January 2007. Yet despite this downside volatility, the Russell 2000® Growth Index has delivered impressive annual returns, averaging 8.63%. during the period from December 31, 2006, through June 30, 2019, providing higher absolute returns than the S&P 500® Index. It’s no surprise why investors are eager to include a sleeve of small growth names in their equity portfolios.

The volatility in small-cap growth is exactly why a disciplined approach to active management within this niche makes sense from our perspective. Often, near-term performance of small, fast-growing companies disconnects from their business outlook. This could reflect the lack of analyst coverage, or perhaps lower levels of liquidity that may exacerbate near-term price movements. Other times, however, falling stock prices truly reflect deteriorating fundamentals. The trick is distinguishing fact from fiction—tuning out the noise as it's often called in the business.

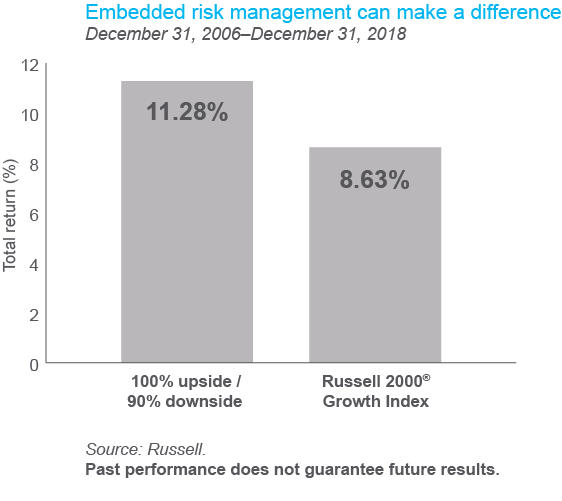

Focusing on stock selection and fundamental research is obviously vital, but having a disciplined risk management process may be the real bedrock of any successful small-cap growth strategy. In fact, at this stage of the economic cycle, an active manager with disciplined risk protocols may be able to minimize the potential negative impact of any individual position and reduce down capture during those inevitable challenging months, which should allow returns to compound at a higher rate over time.

As the adjacent graph illustrates, the asymmetry in up/down capture can be a pathway to outperformance within the small-cap growth space. Even a small improvement in downside capture may help preserve wealth and improve returns over time.

So while small-cap growth investing can be inherently more volatile than some other segments of the equities market, we believe that simply loading up on risk is not the only (or best) way to capture potential alpha. To the contrary, focusing on limiting downside capture may be a potential path to outperformance, even in a higher-growth strategy. This might prove especially valuable in the volatile environment that we see today.