Tech talk: Are sector changes skewing your equities portfolio?

BRIAN JACOBS, CFA 12-Mar-2019

Understanding the changes in the Global Industry Classification Standard (GICS) may seem wonky and of little interest, but don’t be quick to dismiss the minutia. In fact, the recent reclassifications have serious ramifications for technology investors—especially those who have been relying on passive exposure to the tech sector. If not wary, at least be aware.

So what exactly happened? GICS, a standardized classification system for equities, is a default framework for many portfolio managers and index providers to benchmark and classify stocks consistently across different regions and industries. But over time industries change and strategies shift. This past September, GICS created a new Communications Services Sector that merged networking, content providers from the telecommunications, information technology, and consumer discretionary sectors.

According to MSCI, the creator and administrator of GICS, the new Communications Services Sector was created to reflect “the integration between telecommunications, media, and internet companies.” Today, many of these companies offer bundled services such as cable, telephone, and internet services, while others also create interactive entertainment content that can be delivered across multiple platforms. The business models have evolved, so the logic behind reclassifying and creating a new category seems sound. But as always, there are serious ramifications that may be especially meaningful to technology investors.

For starters, Facebook and Alphabet (aka Google), moved to the new communications sector, along with Netflix, Comcast and Disney. Fine. But that also means that any investor who held the largest tech-focused ETFs no longer has exposure to some of the largest technology-oriented companies, such as Facebook and Google. The net result is that many technology index funds and ETFs have changed materially but now have an even greater concentration problem than before.

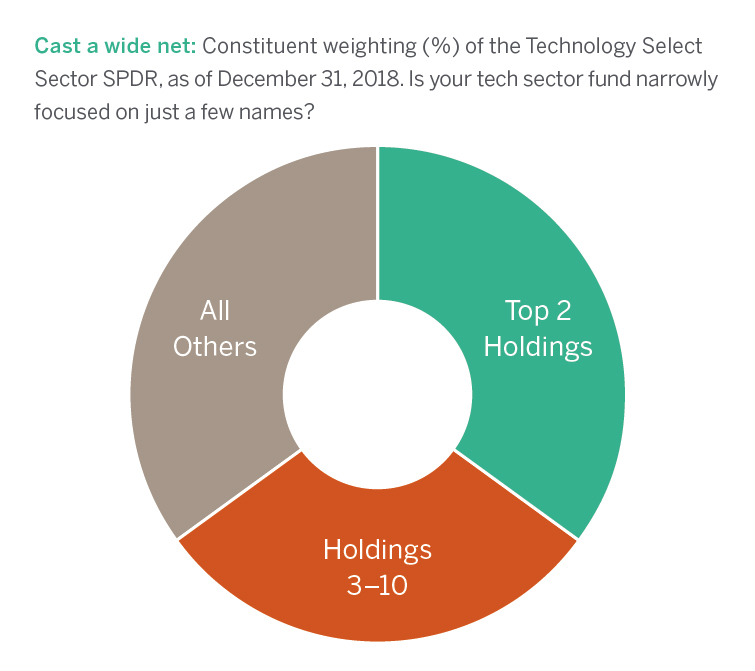

Take the Technology Select Sector SPDR ETF (XLK) and Vanguard Information Technology ETF (VGT), two of the most popular sector ETFs with almost $40 billion in assets as of March 2019. In the case of the Technology Select Sector SPDR ETF (XLK), after the exclusion of Facebook and Google, the ETF is now absurdly overweight to its top two holdings Microsoft and Apple, a concentrated bet that now make up a whopping 37% of the index, while the Vanguard Information Technology ETF (VGT) has an almost a 30% weight to these two names. This is not the diversified, passive approach to technology-oriented companies many investors may think they are taking.

Take the Technology Select Sector SPDR ETF (XLK) and Vanguard Information Technology ETF (VGT), two of the most popular sector ETFs with almost $40 billion in assets as of March 2019. In the case of the Technology Select Sector SPDR ETF (XLK), after the exclusion of Facebook and Google, the ETF is now absurdly overweight to its top two holdings Microsoft and Apple, a concentrated bet that now make up a whopping 37% of the index, while the Vanguard Information Technology ETF (VGT) has an almost a 30% weight to these two names. This is not the diversified, passive approach to technology-oriented companies many investors may think they are taking.

Passive investors should have always recognized that many sector funds are unable to include dynamic companies that are outside traditional tech, as defined by the GICS sector definition. And now they may be forced to skip out on a few of the most dominant large-cap Internet companies as well. This seems arbitrary and wrong.

We think there are better ways to allocate to disruptive and dynamic companies—those with the potential to drive innovation, capture market share, and provide sustained earnings growth. Here are three characteristics that investors should consider before investing in any technology-oriented sector fund:

- Disregard sector labels: Instead of focusing on narrow definitions of technology, look for a fund that offers more diversified exposure to innovation, which is no longer concentrated only among traditional tech stocks. Orienting around innovation can help capture opportunities in biotech and healthcare, in addition to more traditional hardware and software plays.

- Review the portfolio structure: Check the fund’s active share, which is defined as the percentage of holdings in portfolio that differs from the benchmark index. High active share (say, above 80%) illustrates that the manager is willing to stray from the benchmark as a means to capture potential alpha. If your tech fund has a low active share, you may be buying the benchmark (for all practical purposes), which may result in undesired concentration while missing out on many potential opportunities.

- Beware cap weighting: Look for a fund whereby the average market-cap of portfolio constituents is significantly below that of the most widely followed technology index. Tilting the portfolio toward smaller companies ensures that the strategy can allocate capital to innovative tech-oriented companies long before they become household names.