The cavalry has arrived

WASIF LATIF 04-Jan-2020

The first phase of this bear market began on February 20 when we all realized that this virus was a global problem. Then, in early March, the Saudis launched a full assault on oil prices to shake out competitors. Oil prices went reeling and so did the market. Suddenly, the selloff evolved into a massive deleveraging and liquidity panic. As shelter-in-place orders went into effect around the world and businesses closed, the potential economic toll worried all of us. Even the typically stable bond market stopped functioning normally for a spell.

Fortunately, the cavalry came quickly—which is in contrast to what happened in the 2008-09 Global Financial Crisis. The Federal Reserve and other monetary authorities worldwide) leapt into action – cutting interest rates, (re)starting quantitative easing and, in the case of the Fed, launching an array of programs to provide liquidity to stabilize markets.

Image courtesy of Visual Capitalist

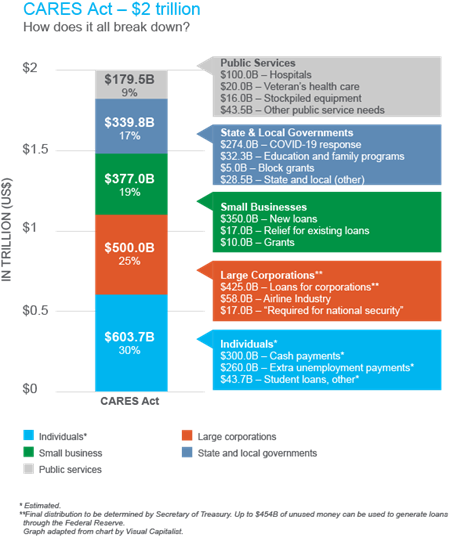

Subsequently, the U.S. government stepped up to provide fiscal support to help corporations, small businesses, and individuals that have been directly impacted. The Coronavirus Aid, Relief, and Economic Security Act (CARES Act) was an excellent first step, and the government continues to debate further measures. This legislation offers something for almost every sector directly impacted by the abrupt economic stoppage.

These steps ended the market’s freefall and helped tighten credit spreads across much of the fixed income universe. In fact, by the end of April the broad market had recovered a substantial portion of its 2020 decline.

But now what? The optimists believe that the economy will recover sooner than later, and in the interim the monetary and fiscal measures provide a bridge to get through this situation. On the other hand, the pessimists—some may say realists—are worried that traders are discounting millions of initial jobless claims, plummeting consumer spending, and terrible PMI data.

Who is right? At this point it’s impossible to tell.

The one certainty in all this murkiness is that elevated volatility—while mercifully well below the peak in March—is likely to continue. Another certainty is that even under the best case scenario, the post-pandemic world will be vastly different and usher in new market leadership. Looking ahead, investors seeking to modify and reposition their portfolios may wish to consider:

- High-quality companies, especially those with a record of increasing dividends over time.

- A tactical allocation approach that allows investors to de-risk a portion of their portfolio when market trends begin to shift, but also with discipline to re-invest when sentiment is overly bearish.

- A relative valuation approach, which might favor domestic small caps versus large caps; emerging markets versus domestic stocks, and value versus growth strategies.

- Alternatives to cap-weighting, such as those that favor risk-weighting.

- Active fixed income strategies that can independently evaluate credit and liquidity risks and take advantage of price dislocations, such as those that arose from recent forced selling.