Think big, act small

GAVIN HAYMAN, CFA JEFFREY KOCHE, CFA BRIAN MATUSZAK, CFA 15-Jan-2020

Could thinking small be the big idea in 2020? In a world mired in relatively low economic growth where headlines seem to be dominated by the corporate giants, investors often wonder where they can tap into the type of growth needed to help build long-term wealth. We have a small suggestion.

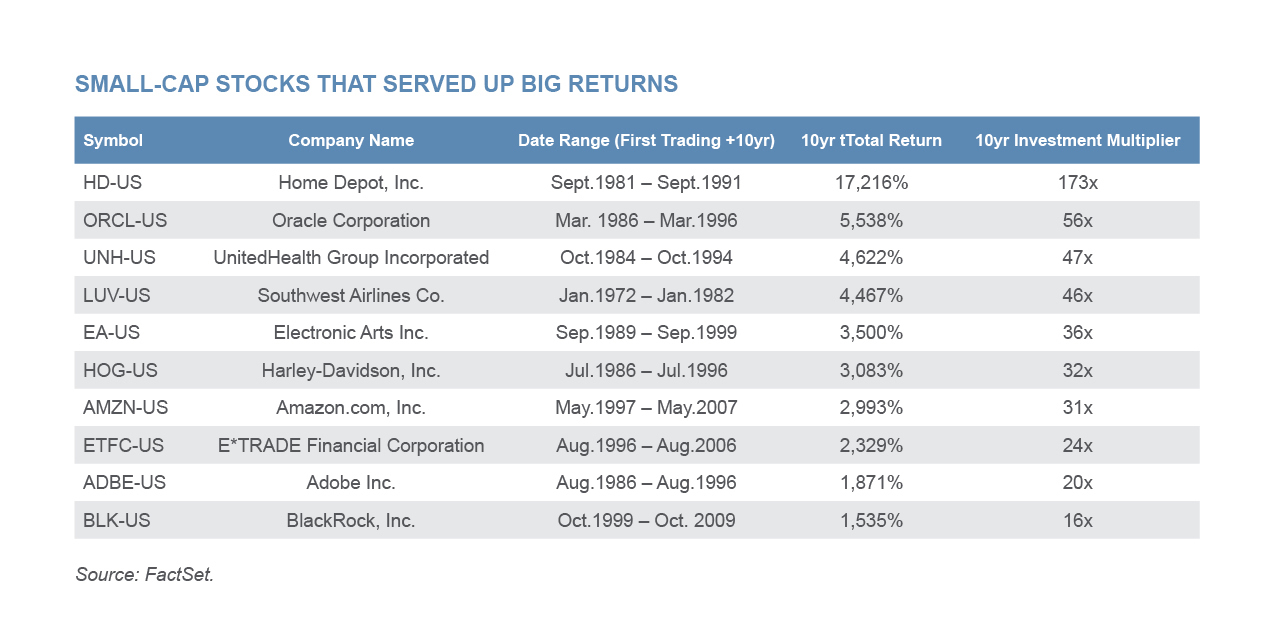

Given where small growth companies are in their life cycle, they have the potential to offer investors dynamic growth opportunities that are harder to find in larger companies. In fact, some of the most well-known large companies today previously enjoyed envious growth rates in the first ten years after their IPOs.

Note: The securities listed above is for illustrative purposes only; the performance shown represents past performance and is not indicative of future results. Victory Capital investment strategies may hold or have held these securities; this chart does not reflect a current or previous recommendation from Victory Capital.

All of the securities listed above were considered small-cap names at their IPOs. As the table shows, within just 10 years after coming public, these stocks increased in value anywhere between 16x to as much as 173x their initial values. These types of outsized returns are much rarer and extremely difficult to find when looking at large caps. Such opportunities no doubt exist, but the challenge is finding them. We believe that a dedicated small-cap manager offers investors the best chance to find tomorrow’s leaders today – and invest in those companies at the most dynamic and rewarding point in their life cycle.

It’s not just the size of the companies that makes this sub-asset class attractive in our opinion. We believe that small caps are more likely to outperform during positive inflections in the economy thanks to the higher cyclicality and beta exposures of smaller companies. Low unemployment, low interest rates, progress on U.S./China trade relations, and our expectations of improving global Purchasing Managers' Indexes—which are indicators of economic trends in the manufacturing and service sectors—are all supportive of stable-to-improving economic conditions. Given that small caps have underperformed their large-cap counterparts recently, we believe that the relative value of small caps has improved materially. This presents an attractive backdrop for small caps in our opinion.

These sentiments are being echoed by investor pundits such as small- and mid-cap strategist Steve DeSanctis of Jefferies and Bank of America Merrill Lynch senior U.S. equity strategist Jill Carey Hall. In a recent Barron’s article, DeSanctis said: “I think small is primed to outperform as the economy and earnings improve in 2020.” Meanwhile, Hall stated: “Small-caps are historically very inexpensive relative to large-caps, even though both are trading above their own histories.” In fact, small caps are one of Bank of America Merrill Lynch’s biggest bullish predictions for 2020, according to that article.