World War "C"

WASIF LATIF 02-Apr-2020

One of the questions I’ve been getting frequently from clients and peers is how this environment stacks up to other crises. Is this like the Global Financial Crisis in 2008, the aftermath of September 11, 2001, the dot.com bust in 2000, or the October 1987 market crash?

In some ways this crisis is like none of those prior ones, and yet it’s like all of them. But to me, the closest parallel may be World War II. Obviously, we are not in a global military conflict, but we are in world-wide fight against an unseen enemy of a global scale. Studying that period may offer us both insight and foresight.

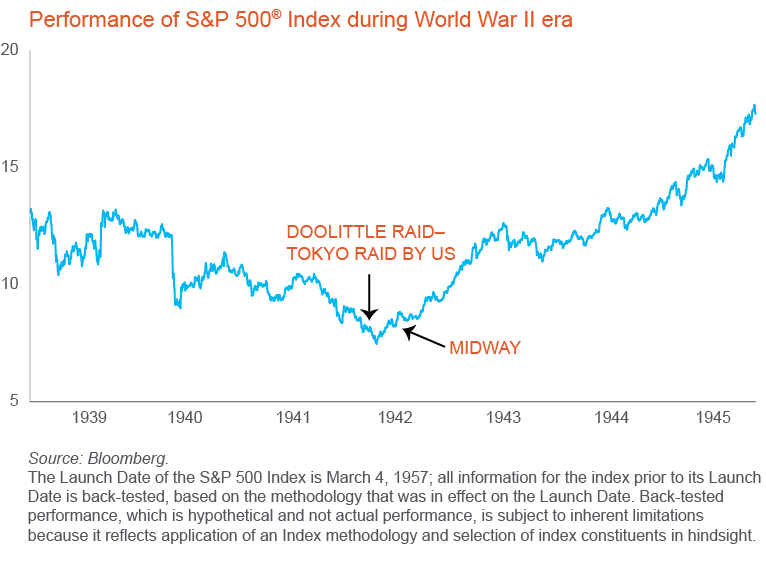

When World War II began in 1939, the S&P 500 Index would shed more than one-third of its value, bottoming in 1942. Counterintuitively, the market didn’t start its march upward when the Allies won the war. Rather, it started rallying once there was a clear path forward towards victory. Historians often cite the turning point in 1942, three years before the war ended, sparked by the Doolittle Raid on Tokyo and followed by the victory at Midway.

Remember, the market is a discounting mechanism that tends to move to extremes driven by fear and greed. Currently, it seems to be reflecting the worst fears of a wholesale economic shutdown. Although the current situation is unsettling, investors need to be on the lookout for the market’s “Doolittle” moment.

Already, the world is fighting the pandemic on four fronts:

Already, the world is fighting the pandemic on four fronts:

- Locally, we are hunkered down and socially distancing in the tiny clusters of our nuclear families.

- On the front lines, healthcare professionals are fighting to save lives, while scientists and researchers are racing to create a vaccine and anti-viral drugs.On the monetary front, central banks everywhere are lowering rates.

- In the U.S., the Federal Reserve (Fed) has already deployed a broad set of new lending facilities and other tools to keep the financial markets from seizing up.On the fiscal front, governments are working to provide near-term support and longer-term stimulus to the halting economy.

- Tax holidays and perhaps even direct cash is on the way to help those most at risk. Of course, such measures will be expensive and have longer-term ramifications for investors, but the need to spark growth is undeniable.

So when this Covid-19 crisis ends—and it will--what will turn out to have been our Doolittle moment? Will it be when the Fed launched its alphabet soup of emergency measures and unlimited quantitative easing in late March? Or is that pivotal moment yet to come?

Nobody knows for certain, but once we see some stability and a way out of this crisis, we expect the market to rally back in anticipation of that recovery. So be ready. And to prepare for that moment, investors may want to consider a few possible portfolio adjustments:

- Focusing on the highest quality companies has historically worked well in this type of environment, including those with a proven record of increasing dividends over time.

- Given the speed and steepness of the selloff, consider rebalancing into stocks and other risk assets in small increments over time (i.e. dollar cost averaging). No need to be a hero and pick the bottom.

- Based on our relative valuation work, U.S. small cap and emerging market stocks look attractive relative to U.S. large caps.

- The unprecedented volatility in fixed income makes a strong case for actively managed fixed income strategies that independently evaluate credit and liquidity risks. Perhaps more importantly, an active manager can take advantage of opportunities that arise from fear and forced selling.