Active vs. passive: It's not binary

MANNIK DHILLON, CFA, CAIA 23-Aug-2018

In the real world, most decisions you face are not binary. Why should that be any different when it comes to building a portfolio? So with regard to the age-old active versus passive management debate, I don’t think it’s a simple either-or proposition. Significantly more nuance and contemplation is required. Rather than a focusing on labels, astute goals-based investors should step back to:

- consider near- and long-term investment objectives and

- determine how different approaches can work in tandem to move toward those goals

Only in such a holistic context can investors begin to assemble portfolios with the appropriate building blocks (i.e. investment products) that may offer the greatest probability for success. In all likelihood, investors will find that there’s room for both passive and specialized active strategies, as well as some potentially promising approaches that bridge the gap between the two.

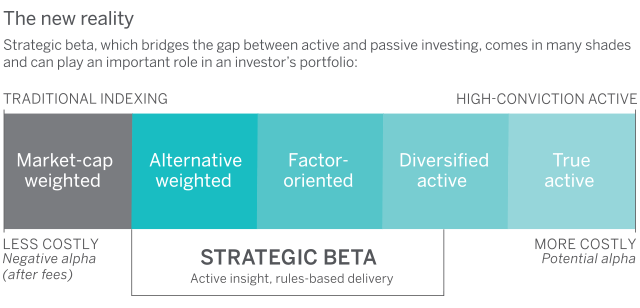

One such blended approach that’s gaining popularity, and in some cases notoriety, is strategic beta. Often called smart beta, it refers to a group of indexes and related investment products that aim to provide an alternative to traditional market-cap weighting strategies of passive investments.

The strategic/smart beta category has grown rapidly due to its potential to deliver on the coveted benefits of skilled active management, primarily alpha¹ generation and risk reduction, but in a wrapper that also has some of the attractive attributes of passive approaches, not the least of which are low relative costs. It’s easy to see why investors might be interested in these investments.

However, it’s important to remember that strategic beta is not “one” thing. It should not be viewed as an asset class. In reality, the strategic beta umbrella covers a diverse array of approaches. Used appropriately, it has the potential to effectively supplement both skilled active management and traditional passive strategies that may help solve for any number of vexing investor challenges. But care is required because allocating to strategic beta is not a simple asset allocation decision. Rather, selecting individual strategic beta products and incorporating them in a portfolio is a careful process made in the context of specific investor goals and risk budgets.

Remember, investors always are trying to balance three critical components: return, risk, and cost. In terms of returns, more is better. In terms of risk and costs, less is more. By providing a disciplined, active-like approach to passive investing that balances return, risk, and cost, strategic beta may provide transparent exposure to a portfolio of preferred factors² and intuitive tilts. And as a strategic tool, it may enhance a passive allocation and counterbalance some of the inherent biases and other limitations of traditional cap-weighted indexing, while striving to deliver alpha at lower costs than active strategies.

Thus the ability to bridge the gap between active and passive explains the appeal of strategic beta. Of course it’s important to reiterate here that the strategic beta universe covers an array of investment philosophies, so before incorporating it into a portfolio, investors must understand the rules, underlying approach and objectives used by each strategic beta product. Arbitrarily trying to fill an allocation bucket with random strategic beta funds can have unwanted ramifications. Such a short-sighted approach could skew the portfolio with sector biases or inadvertently double down on unintended factor exposures. That said, in the right circumstances and after careful due diligence, I believe that certain strategic beta strategies could prove helpful in an investors’ portfolio.