Drop the barbell: Mid-cap stocks do the heavy lifting

BRIAN JACOBS, CFA 06-May-2019

Investors who have adopted a barbell approach for domestic equities—i.e., focusing primarily on the far ends of the capitalization spectrum—may be missing the potential benefits offered by mid-cap stocks. We believe there are compelling reasons to consider making a deliberate allocation to mid caps, not the least of which is performance potential.

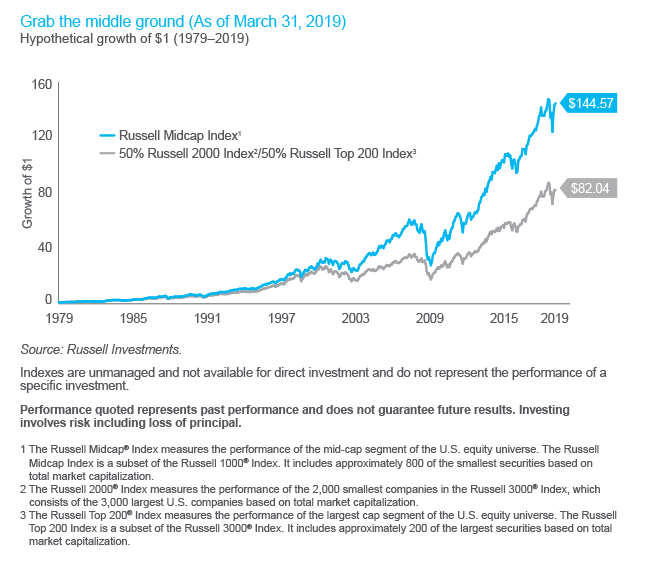

Consider that a pure allocation to mid caps has outperformed a barbell approach (50% large-cap stocks, represented by Russell Top 200® and 50% small-cap stocks, represented by Russell 2000®), over the long term. In fact, a $1 investment in mid caps in 1979 would have grown to over $144 today, as of March 31, 2019. That same investment in a barbell portfolio of half small caps and half large caps (using the representative indexes above) would have grown to slightly more than $82 during the same period, albeit that’s an improvement over either a stand-alone investment in the Russell 2000 Index that would have netted $77 or a stand-alone investment in the Russell Top 200 Index that would have grown to $76.

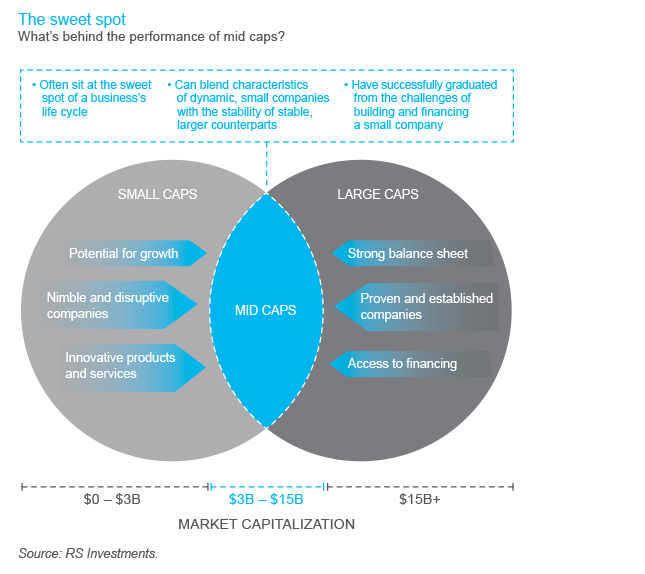

So why, exactly, have mid-cap stocks have consistently surpassed their small- and large-cap counterparts? The reasons could be related to some of the inherent benefits that these companies enjoy given their maturity and size. For starters, these companies are neither illiquid micro-caps, nor global behemoths. They are, however, vetted and well-established, with proven products and services. They generally are less risky than developmental-stage companies but still offer a long runway of potential growth. Some companies also have characteristics that make them less economically sensitive and more apt to capture durable return streams and market share. In addition, these companies can be ideally situated at the sweet spot of the business cycle, blending the characteristics of dynamic small companies but with stability and access to capital of large caps. And in certain sectors, mid caps may benefit from the tailwind of M&A activity.

Another intriguing advantage for the mid-cap asset class is that fact that while many of the underlying businesses are relatively mature, they don’t face the law of large numbers that challenges large growth companies. So, when you begin with a group of proven companies, which is exactly what most mid caps are, it’s likely you are looking at a subset of high-quality businesses with good cash flows, margins, and returns on capital. From there, a growth manager can look for innovative companies with competitive advantages and sustainable growth prospects. Sometimes that’s the result of a new product or technology, or maybe it’s a disruptive approach to delivering an established service. Regardless, it’s an ideal universe from which an active manager can pick stocks and hunt for alpha precisely because many investors overlook mid caps in favor of the barbell approach. As a result, the market for mid caps is not as efficient as it could be.

Of course valuation always matter, especially with quality companies that can sometimes get bid up because they are so appealing. That’s why it’s important to maintain discipline and not allocate blindly—as in an arbitrary passive approach—because there’s a difference between a good business, and what looks to be a good stock for the next three to five years.