Exit stage left: When mega-caps fall out of favor

DAN BANASZAK, CFA 20-Feb-2019

If you were to flip on your favorite financial news site, the odds of hearing mention of Facebook, Apple, Amazon, Netflix or Google are close to 100%. Indeed, there’s no shortage of media attention heaped on the mega-cap darlings of the S&P 500® Index. We even have pet names – FAANG, for example – to make it easy and trendy to reference these stocks.

But remember, the largest stocks in a cap-weighted index are not permanent fixtures, and the spotlight will not always shine brightly on them. So when mega-caps fall out of favor, they will act as a performance anchor for any passive investment that tracks the index. That’s just how cap-weighted indexes like the S&P 500 work.

Given that reality check, investors may want to question whether these popular stocks merit an overweight investment. Another way of putting this: Do the mega-cap headline-grabbers of today represent the best opportunity for our investing dollars in the future?

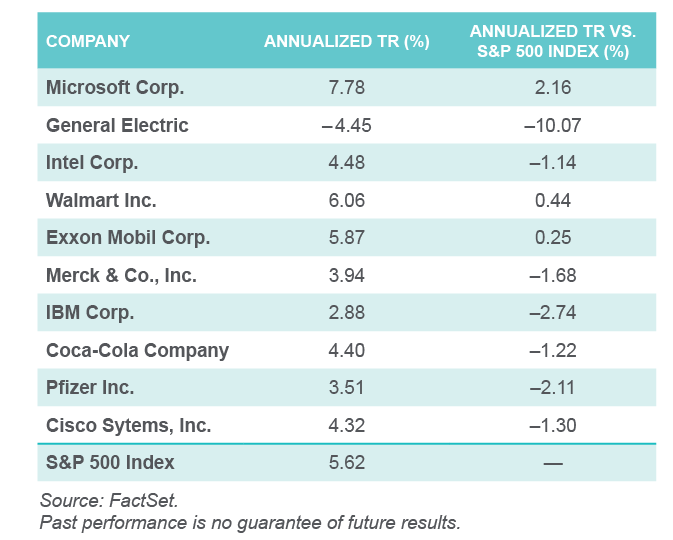

To answer this question, we look at the mega-cap stocks of yesteryear and see how they have performed (and changed) over time. The table below shows the 10 largest stocks in the S&P 500 as of 20 years ago and their annualized total return, as of December 31, 2018:

Only three out of the 10 largest stocks in the S&P 500 in 1998 produced a larger total return than the S&P 500 over the subsequent 20 years. Of these three, only Microsoft materially outperformed the entire index. The remaining seven stocks all underperformed the S&P 500 by at least a full percentage point, annualized. Even GE—once considered one of the brightest and most diversified stars in the index—has fallen on hard times and would have lost almost 60% of your starting investment during that 20-year stretch.

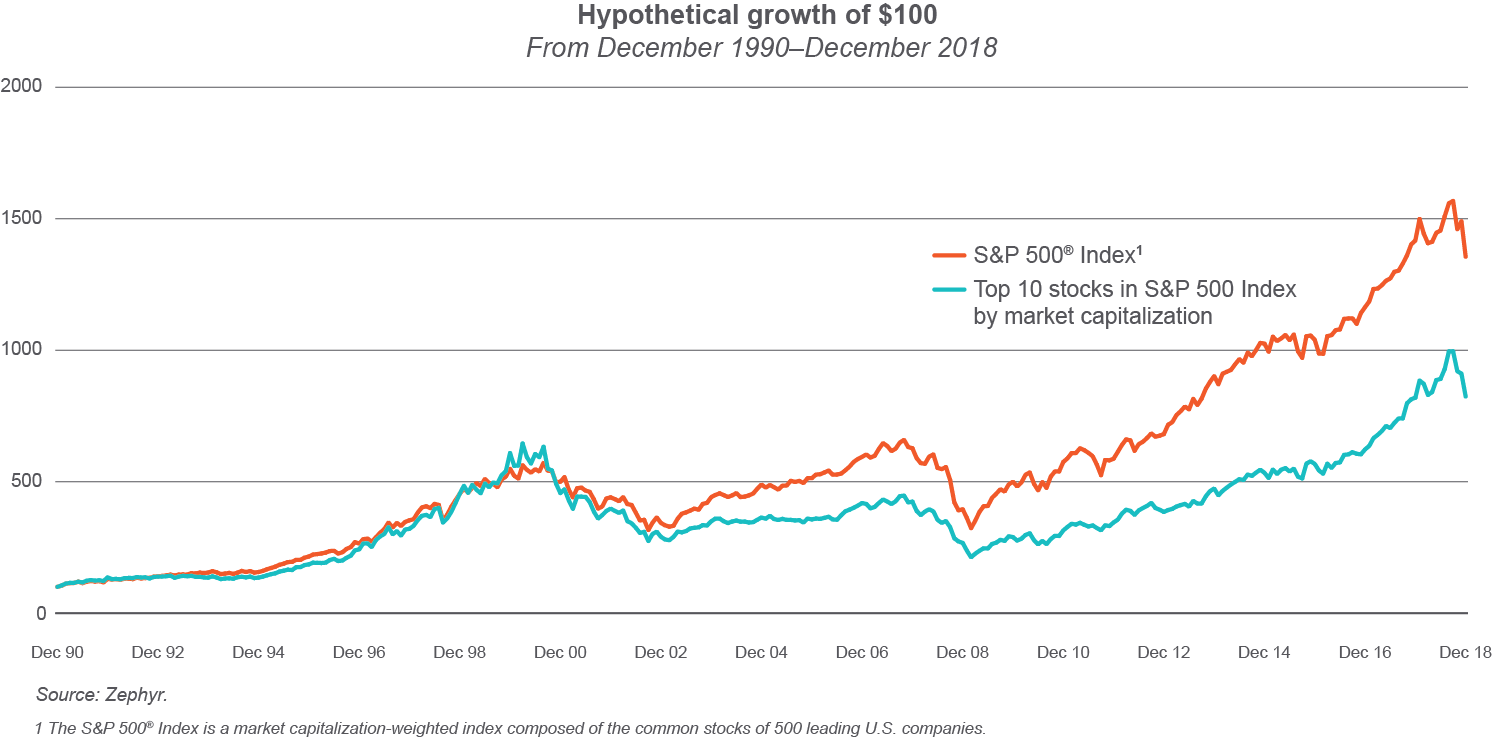

If you still think that following the cap-weighted S&P 500 is the best way to make a large-cap allocation, consider looking at the composite performance of the top 10 stocks in the S&P 500 over time. The chart below shows cumulative returns of the 10 biggest market caps in the S&P 500 (rebalanced quarterly) versus the entire index:

Again, the mega-caps don’t shine so brightly in this light. Since 1990, the top 10 stocks as a group have underperformed the S&P 500 index by more than 190 basis points annualized. A starting investment of $100 in the top 10 stocks alone would have grown to $824, while that same $100 would have grown to $1,356 for the entire index.

To put this in context, let’s look back at the best performing stocks of the last 20 years. Out of the 100 highest returning stocks of the S&P 500 of the last 20 years, the following emerges:*

- Only one of the 100 highest-returning stocks was in the 50 largest market caps of the S&P 500 in 1998.

- Of the 100 best performing names in the S&P 500 over the last 20 years, almost one-third (31) weren’t even in the S&P 500 index 20 years ago.

In summary, mega cap stocks may continue to outperform in the short term, as they have in recent years. The media can continue to give them cute acronyms. And investors can follow the all the nuances of today’s hot mega-cap technology stocks. But remember, these darlings may not always outperform. Spreading risk (and capital) more evenly across all constituents may prove to be a better approach for a core equities allocation than fixating and over-allocating to mega-caps.