Hitting the wall: What's next for emerging markets?

MIKE REYNAL 19-May-2019

Over the past few days, trade talks between the U.S. and China hit the (Great?) wall and ultimately broke off. Subsequently, the U.S. announced additional tariffs of up to 25% on $300 billion worth of Chinese imports. China, of course, responded with $60 billion worth of tariffs on an array of goods and services. Not surprisingly, the equity markets did not like this escalation in the U.S.-China trade dispute, and emerging markets investors once again found themselves in the cross-hairs.

This situation is dynamic, and we do not know when or how it will be resolved in the near term. Nobody does. What we do know, however, is that volatility will likely continue with each tweet out of Washington and each soundbite out of Beijing. That’s a virtual certainty, so buckle up.

During times like this when the situation is murky and the disquieting headlines only exacerbate matters, it’s important to look at the facts. And the one overarching fact is that the interests of world’s largest and second largest economies are aligned. Nobody wins a long-term trade war.

For starters, globalization continues to help China’s companies grow and boost productivity by gaining access to new markets, tapping new sources of talent and strategic assets, and creating competitive pressure in domestic industries. Of course changing the framework for forced technology transfers and reducing the level of market-distorting industrial subsidies within China are key concerns for U.S. firms. But it’s also important to remember that U.S. companies are likely to be affected by any prolonged trade tensions given that so many imports from China are capital and intermediate goods. China may need a trade deal, but U.S. companies also cannot afford a long-term disruption to their supply chains.

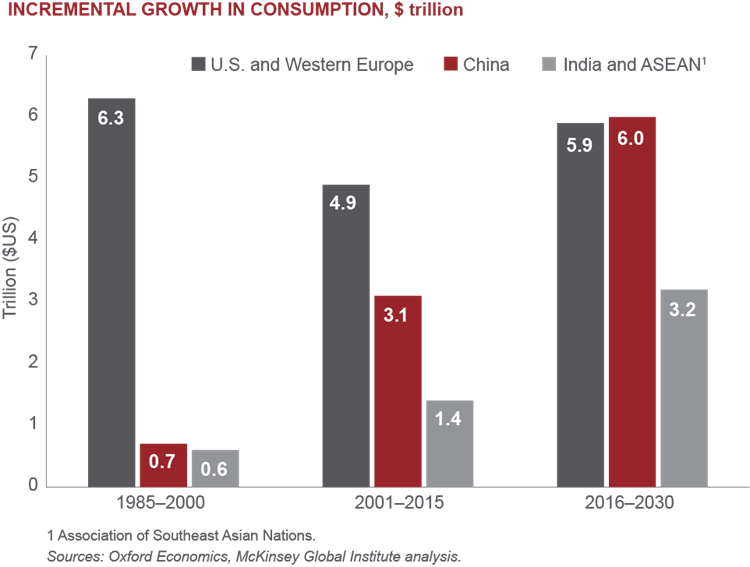

Finally, China’s projected consumption growth over the next 15 years might best illustrate why there’s likely to be an amenable resolution soon. U.S. companies want (need) access to new markets, and they do not plan to miss out on the exciting opportunity to sell into such robust consumer growth potential.

President Donald Trump and President Xi Jinping are both expected to attend the G20 summit on June 28 and 29, and it’s quite possible, even likely, that we will see ongoing posturing by both countries prior to that meeting. Still, we believe there is motivation for both sides to get a deal done.

In the interim, we believe that China could respond with some stimulus or policy changes that may provide material benefits to many mid- and small-cap Chinese companies. And if volatility creates an even larger disconnect between share prices and individual company fundamentals, we aim to be ready for any potential buying opportunity.