Is history about to rhyme?

DANIEL G. BANDI, CFA 08-Mar-2020

Mark Twain is often credited with the famous quote: “History doesn’t repeat itself, but it often rhymes.” Whether he said that or not, is one thing. More important is what history can tell us about investing and, specifically, the viability of value-oriented strategies in 2020.

Harken back to the mid-1930s when the economic insecurity caused by the Great Depression set off waves of social tension that, in many regards, appear to be repeating (or at least rhyming) in our current environment. Not coincidentally, this comes just one decade removed in the aftermath of the Great Recession of 2008.

These social trends are interesting, but even more meaningful may be the parallels drawn when comparing the historical performance of small-cap value investing to small-cap growth using Fama-French data.

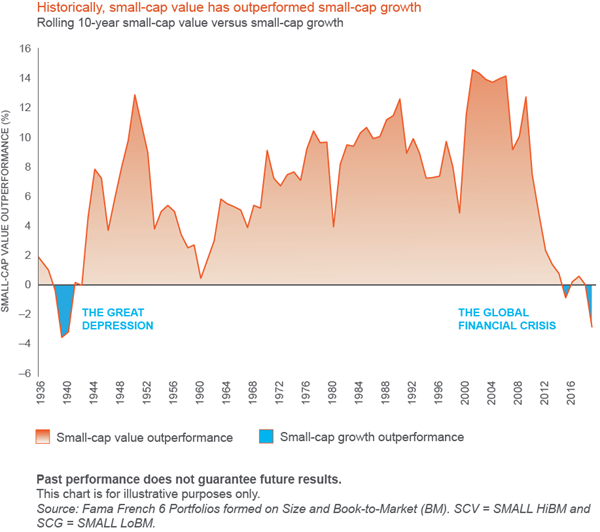

Many investors may be surprised to learn that dating back to 1927 (which is as far back as data is available), small value actually has outperformed small growth the majority of the time over one-, three-, five-, and 10-year periods. In fact, small value has outperformed small growth 59% of the time on a one-year basis, 73% on a three-year basis, 80% on a five-year basis, and 93% of the time on a 10-year basis.

Of course most investors are better at remembering the most recent history of small-value strategies getting trounced by small growth. But given our longer-term, historical perspective, we were wondering if the current streak of growth outperformance is unusual or if it has precedent.

What we found was quite interesting. The current outperformance of small growth versus small value is now the longest since the Great Depression. On a rolling 10-year basis, small value has outperformed only two times out of the last 10 years. But as it turns out, this is an aberration from historical precedent. In fact, the past decade is the worst 10-year relative performance of small value versus growth since 1927.

Naturally, the next question for investors is whether this trend of small growth beating small value can continue, or has it gone too far? Will 2020 see a style rotation and become the year of small value?

We don’t have a definitive answer to that question—no one does. What we do have, however, is conviction that an allocation to small-value strategies has merit over the long term. So while small growth has outperformed small value over the last three years, it has only had one stretch of four-year outperformance, and that was way back in 1937–1940.

There has been much talk of the death of value investing in the financial media, but we believe that investors should be careful about complacency and believing that trends are destiny. Betting against small value today is paramount to taking a very rare historical bet. Will small growth complete an unparalleled reign over small value, or will we see reversion to the mean? Obviously, we are biased as value-oriented investors, but time will tell.